![Monitor-1-istockphoto-1437090010-612x612-3[1]](https://sustainablest.wpengine.com/wp-content/uploads/elementor/thumbs/Monitor-1-istockphoto-1437090010-612x612-31-1-r9s7e2aed1qqg9yi2cpd239lst9qqb7mxo8vlrrwks.jpg "Monitor-1-istockphoto-1437090010-612×612-3[1]")

The Bottom Line: Sustainable fund assets expanded with the benefit of capital appreciation, fund launches remained anemic while the relative performance of ESG indices rebounded.

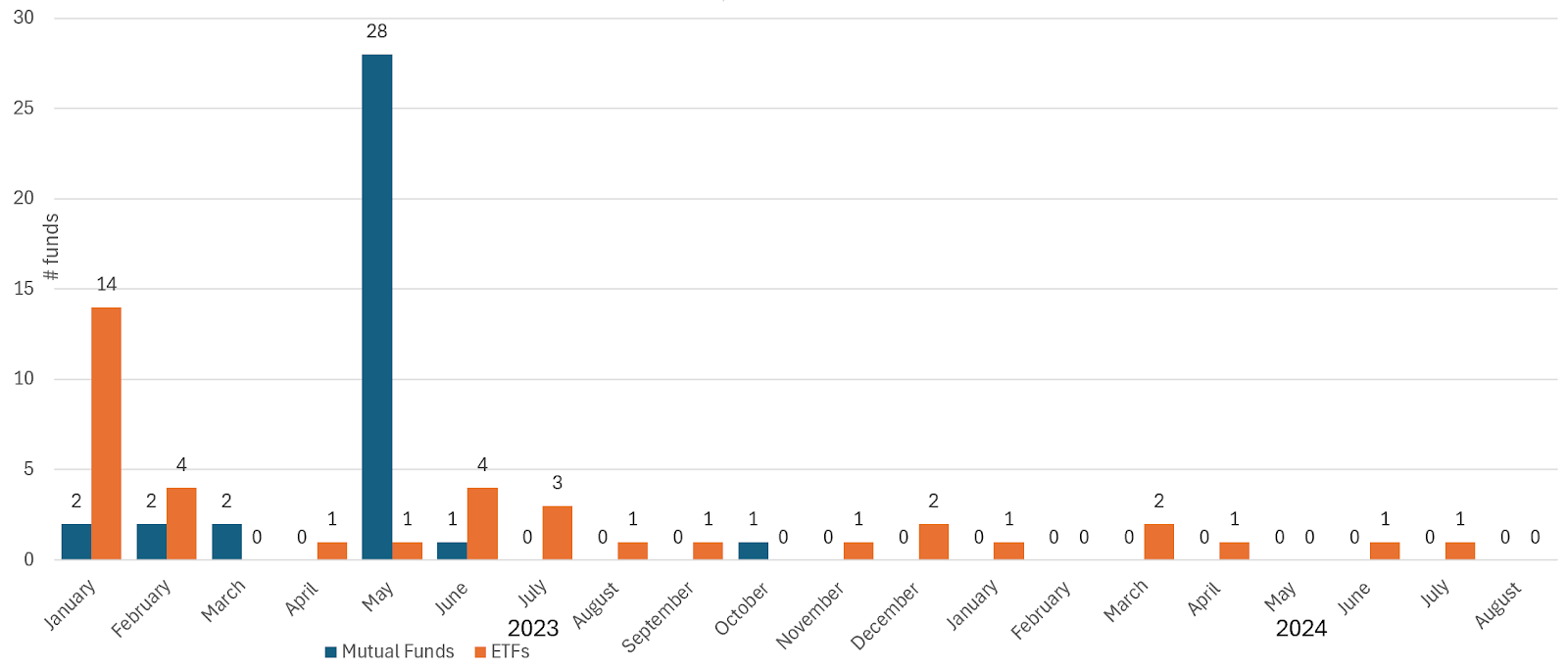

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

Focused sustainable long-term fund assets under management attributable to mutual funds and ETFs (excluding money market funds), 1,433 funds/share classes in total, based on Morningstar classifications, closed the month of August with $355.9 billion in net assets. This represents a net increase in the amount of $6.5 billion, or a gain of 1.9%, versus a slightly higher $6.6 billion in the previous month. This is now the highest month-end assets level achieved so far this year and above any month-end levels achieved in 2022. The net assets of both sustainable mutual funds as well as ETFs also reached new month-end high levels in August, attributable largely to capital appreciation. Based on a simple calculation that reflects the average August total return gains recorded by long-term mutual funds at 1.9% and 1.5% by ETFs, it is estimated that sustainable funds experienced cash outflows during August in the amount of about $0.2 billion to $0.3 billion, largely attributable to capital appreciation and modest inflows into ETFs that were offset by slight mutual fund outflows. Since the start of the year, focused sustainable mutual funds and ETFs have added a combined net of $24.2 billion in net assets, for an increase of 7.3%. Mutual funds accounted for about 70% of the gain. |

New Sustainable Fund Launches |

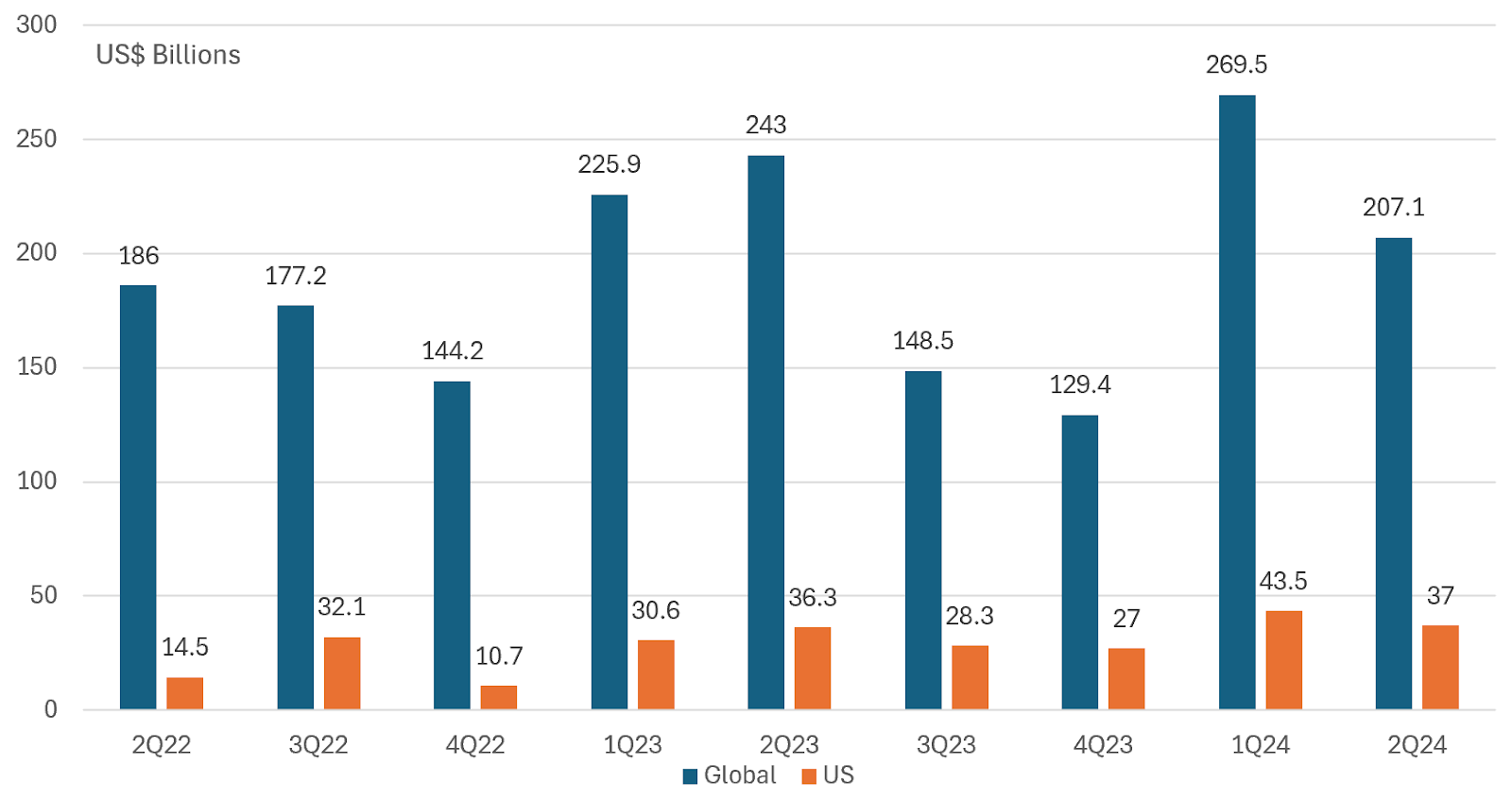

There were no new mutual fund or ETF launches in August, reflecting a continuing drought in sustainable fund launches. During the eight-month interval to the end of August, a total of six fund launches were recorded, all ETFs (this reflects an revised to reflect the launch of a new ETF in July). This record stands in sharp contrast to the 63 funds that were launched during the comparable period in 2023. Liquidations affected six mutual funds and two ETFs. Four BlackRock managed mutual fund liquidations were reported, with assets totaling about $104 million, largely attributable to institutional investors, perhaps in the form of seed commitments. At the same time, two ETFs were liquidated, including the $25.5 million BlackRock Future Climate and Sustainability Eco ETF and the $3.2 million Veridian Climate Action ETF. It seems that the fund “could not conduct its business and operations in an economically efficient manner over the long term due to the Fund’s inability to attract sufficient investment assets to maintain a competitive operating structure.” That said, the Chief Investment Officer and portfolio manager of the fund’s sub-adviser’s resigned without further explanation. The scarcity in sustainable fund launches, starting after May of last year, may be attributable to the fact that anti-ESG movement in the US had gained momentum in the second quarter of 2023 and fund companies may have opted to lower their profile by curtailing focused fund offerings. While this may be the case, a just released Bain & Company research report entitled The Visionary CEO’s Guide to Sustainability 2024 indicates that sustainability remains important to corporate executives even as the importance of sustainability has declined. At the same time, roughly 60% of 19,000 consumers surveyed say their concerns about climate change have increased in the past two years. |

Green, Social and Sustainability Bonds Issuance (to Q2 2024) |

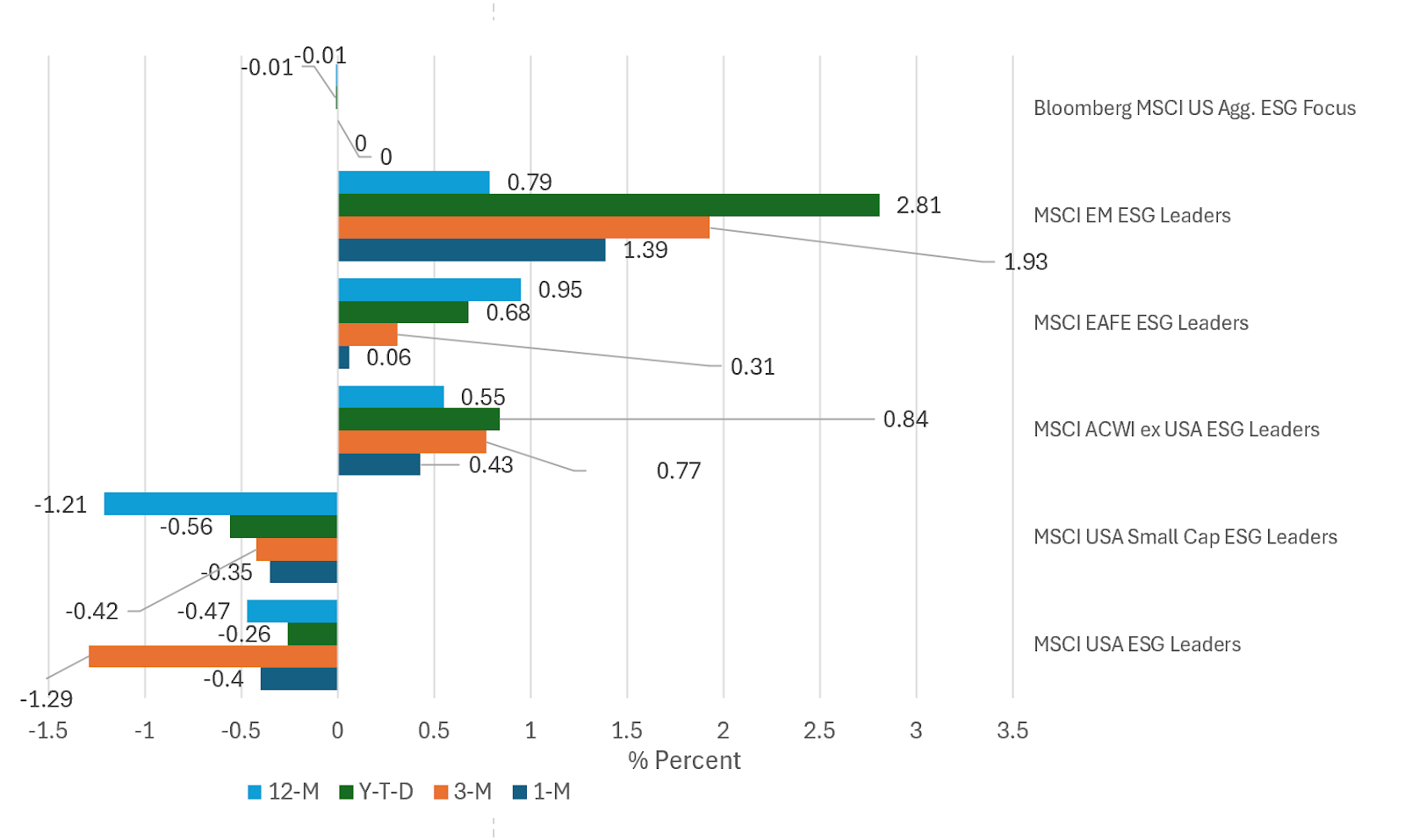

The latest available data according to SIFMA show that global green, social and sustainable bond issuance in the second quarter of 2024 reached $207.1 billion. This represents a quarter-over-quarter decline of $62.4 billion, or a decline of 23.2%. Green bonds accounted for 68.3% of global issuance while sustainability bonds and social bonds represented 19.7% and 12.0% of total issuance. Global issuance year-to-date reached $476.6 billion versus $468.9 billion over the comparable period in 2023. This represents a slight $7.7 billion pick up in sustainable bond issuance, or an increase of 2%. US sustainable bond issuance in the second quarter registered $37.0 billion, down $6.5 billion from $43.5 billion issued in the first quarter 2024, or a 2% decline. That said, June saw a slight pickup in issuance, increasing from $11.9 billion to $13.2 billion. It should be noted that SIFMA data tends to understate global sustainable bond issuance as it captures a narrower slice of the market that also includes sustainability linked bonds and notes, for example. More generally, sustainable bond data provided by different data sources can vary by significant margins. Last year, for example, UNCAD reported that global green bond issuance reached $872.2 billion while Bloomberg reported an even higher $939 billion versus $746.8 million compiled by SIFMA. |

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

After a sharp stock sell-off at the beginning of August affecting the S&P 500 index as well as other major stock market indices, markets rebounded in response to positive economic data on inflation and retail sales that helped calm recession fears and a signal by the Federal Reserve that it was ready for interest rate cuts. For the full month, the S&P 500 registered a total return gain of 2.4% and 27.1% over the trailing 12-months, the NASDAQ 100 gained 1.2% and expanded the twelve month gain to 27.3% while the small cap Russell 2000 index, whose momentum may have faltered, dropped 1.5% and recorded a trailing twelve month gain of 18.5%. The best performing large cap sectors included Consumer Staples, Real Estate and Health Care, up 5.8%, 5.6% and 5.0%, respectively, while Real Estate and Health Care also ranked in the top three sectors of the mid-cap and small cap indices. Against this backdrop, focused sustainable mutual funds and ETFs, a combined total of 1,446 funds and share classes with $360.6 billion in assets under management, registered an average increase of 1.8% in August and an average 15.4% over the trailing twelve months. Sustainable international equity funds led with an average gain of 2.4% while US equity funds added an average of 1.9%. A selection of five US and international equity ESG Leaders indices and one fixed income benchmark, for a total of six benchmarks constructed by MSCI around ESG screening and exclusionary criteria, bounced back in August. Of the five equity-oriented ESG Leaders indices, the three foreign indices led their conventional counterparts over the 1-month, 3-month, YTD and trailing 12-month intervals. For the month of August, the MSCI Leaders ACWI ex USA ESG Index, EAFA ESG and Emerging Markets ESG led their conventional counterparts by levels ranging from a low as 43 bps to a high of 139 bps. However, their US large-to-medium cap as well as small cap counterparts achieved the opposite results in that they lagged over the four time periods up to 12-months. In August the MSCI USA ESG Leaders Index and USA Small Cap ESG Leaders Index fell behind their conventional counterparts by 4 bps and 35 bps, respectively. At the same time, the Bloomberg MSCI USA Aggregate ESG Focus Index came in even relative to the underlying Bloomberg US Aggregate Bond Index. Over the intermediate and long-term time frames, relative results through August have been faltering. Evaluated over three time periods, from three years to ten years, the best interval, over the five-year period, produces a 50% level of outperformance relative to conventional benchmarks. Over the three-year interval, only one benchmark, the MSCI USA ESG Leaders Index, managed to outperform its conventional counterpart. It did so by an annualized average 74 bps. |

Sources: Morningstar Direct, MSCI, SIFMA/Dealogic, various fund prospectuses and Sustainable Research and Analysis LLC