The Bottom Line: Sustainable fund assets expanded due to capital appreciation, fund launches remain moribund, sustainable bond volume dips and ESG indices reflected mixed results.

|

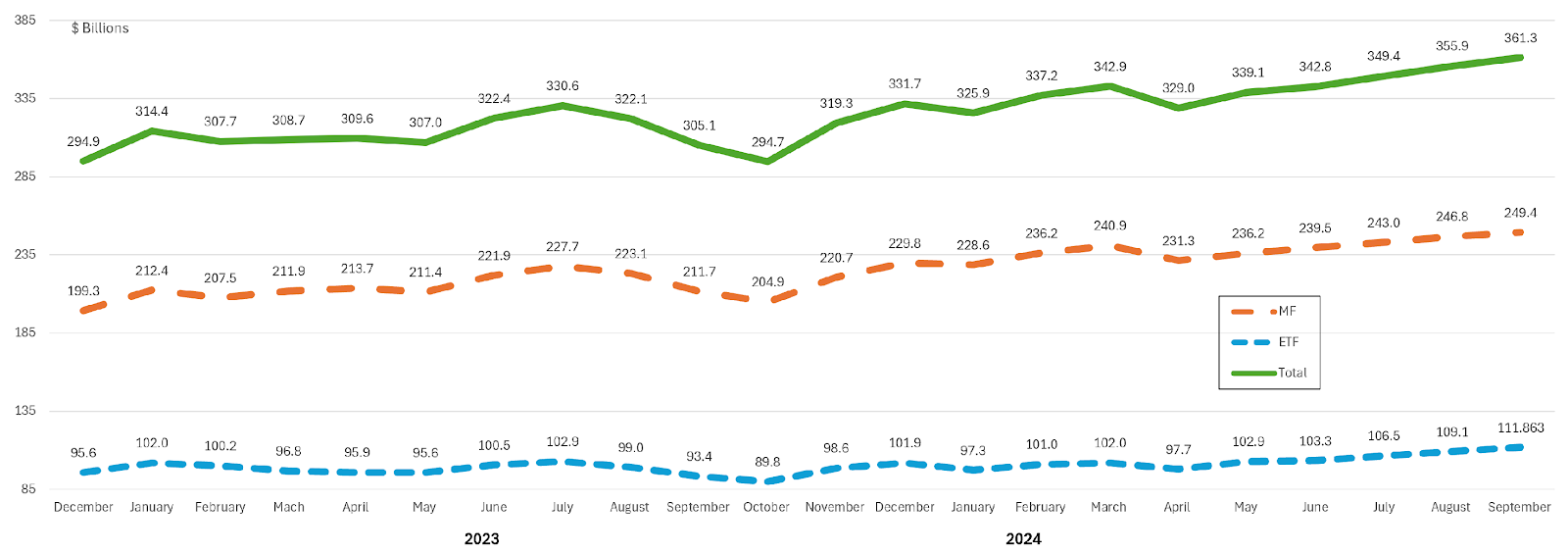

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

|

Focused sustainable long-term fund assets under management attributable to mutual funds and ETFs (excluding money market funds), 1,412 funds/share classes in total (1,175 mutual funds/share classes and 237 ETFs), based on Morningstar classifications, closed the month of September with $361.3 billion in net assets. This represents a net gain in assets of $5.4 billion, or an increase of 1.5%. The monthly net gain was the lowest in the third quarter, trailing the $6.5 billion uptick in August and $6.6 billion in July. Still, net assets in September reached the highest month-end assets level achieved so far this year and above any month-end levels recorded in 2022. The net assets of both sustainable mutual funds as well as ETFs also reached new month-end high levels in September, attributable entirely to capital appreciation of about $5.4 billion. Based on a simple calculation that reflects the average September total return gains recorded by long-term mutual funds at 1.8% and 3.05% by ETFs, it is estimated that sustainable funds experienced cash outflows during September in the amount of about $2.3 billion. Mutual funds experienced cash outflows estimated at $1.7 billion while ETFs registered outflows estimated at around $600 million. Since the start of the year, focused sustainable mutual funds and ETFs have added a combined net of $29.6 billion in net assets, for an increase of almost 1%. Mutual funds accounted for about 70% of the gain. |

|

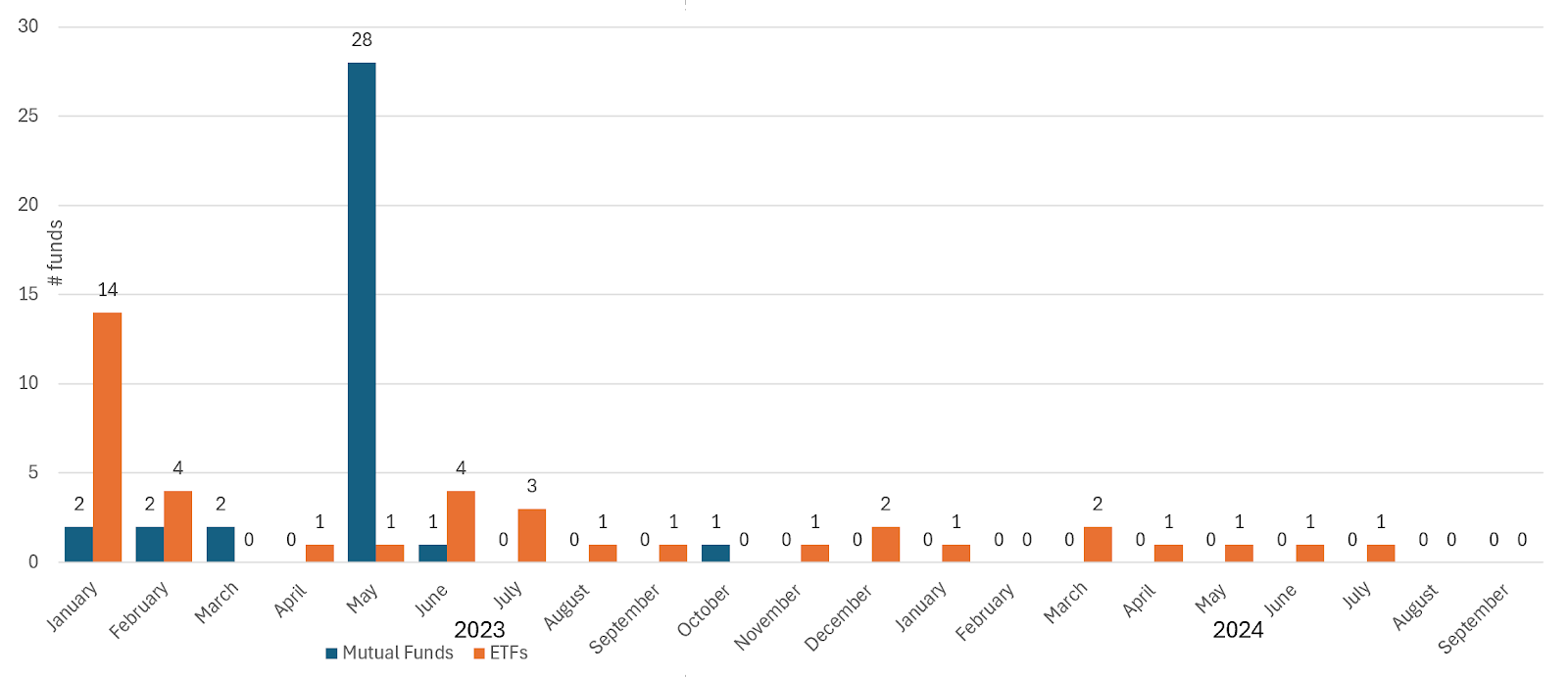

New Sustainable Fund Launches |

|

The drought affecting new listings of focused sustainable funds, which started after May of last year, continued into September 2024. There were no new mutual fund or ETF listings during the month, while during the third quarter, only one new ETF was launched versus five new funds during the same period last year and a total of only seven funds (adjusted), all ETFs, launched since the start of the year versus 64 during the same period last year. The only fund launched in the third quarter is the $300 million KraneShares Sustainable Ultra Short Duration Index ETF (KCSH) that, in addition to its fundamental investment strategy, invests in securities that are compatible with the principal objective of the Paris Climate Agreement, which seeks to limit temperature increases in this century to well below 2 degrees Celsius, preferably to 1.5 degrees Celsius, above pre-industrial levels (i.e., carbon reduction target levels) while also employing exclusionary screens based on certain business practices. During the month, there were two fund liquidations (excluding fund share classes). These included the $3.9 million Blue Horizon BNE ETF and the $16.3 million AMG GW&K Enhanced Core Bond ESG Fund with its three share classes. The scarcity in sustainable fund launches, starting after May of last year, may be attributable to the fact that anti-ESG movement in the US had gained momentum in the second quarter of 2023 and fund companies may have opted to lower their profile by curtailing focused fund offerings while at the same time continuing to support sustainable investing practices. Sustainability also remains important to corporate executives as well as asset owners. According to a just released Voice of the Asset Owner Survey 2024 report by published by Morningstar based on survey findings, 67% of asset owners globally say that “ESG has become more material in the last five years.” |

|

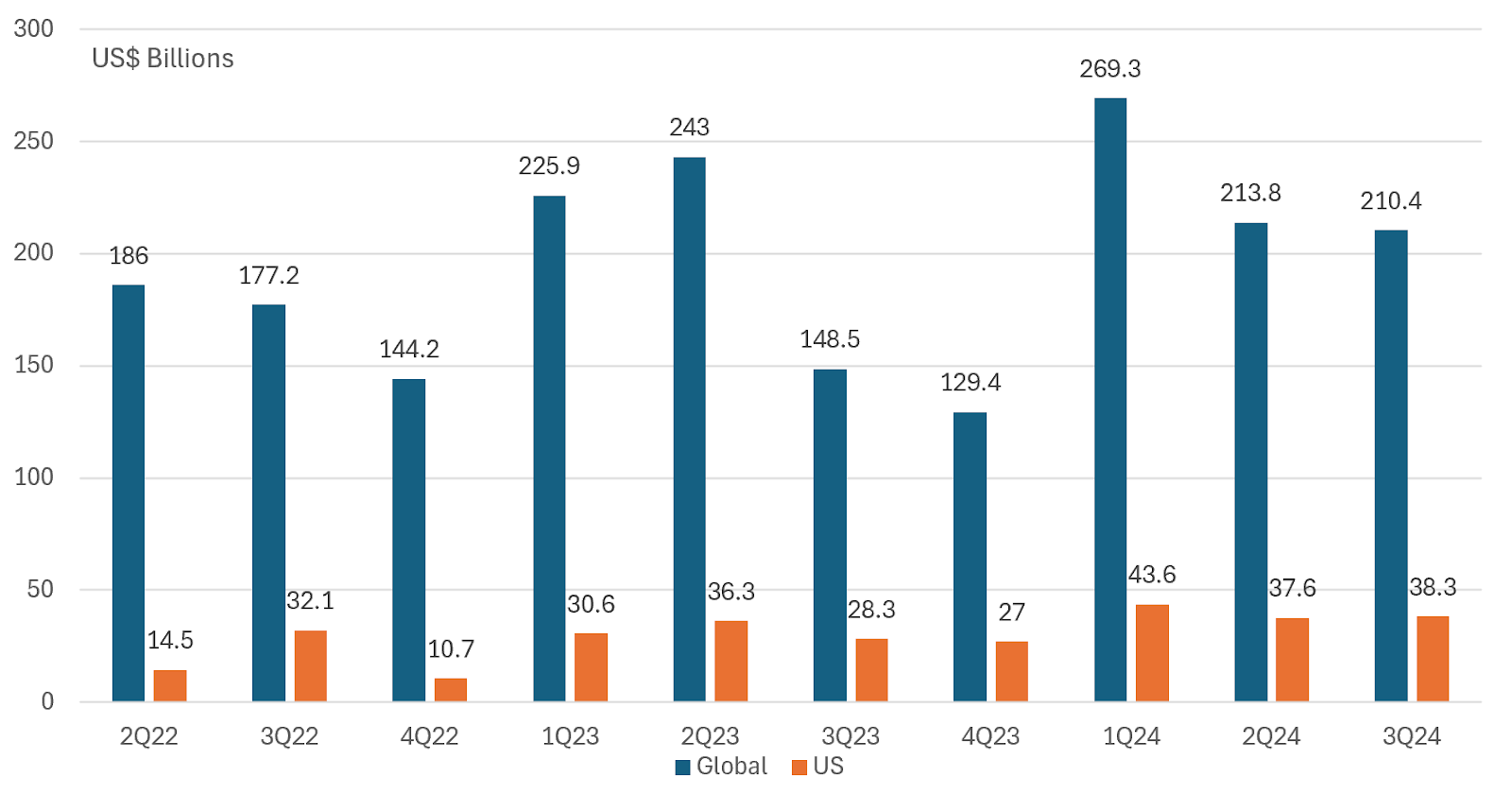

Green, Social and Sustainability Bonds Issuance (to Q3 2024) |

|

In the just released third quarter data according to SIFMA, global green, social and sustainable bond issuance in the third quarter of 2024 reached $210.4 billion. Based on slightly adjusted issuance numbers for the second quarter, this represents a quarter-over-quarter decline of $3.4 billion, or a 1.6% drop. Green bonds accounted for 57.9% of global issuance while sustainability bonds and social bonds represented 25.4% and 16.7%, respectively, of total issuance. Global issuance year-to-date reached $693.5 billion, running ahead of the comparable period last year when volume reached $617.4 billion or over the comparable period in 2023. This represents a $76.1 billion pick up in sustainable bond issuance, or an increase of 12.3%. Against a backdrop of another strong quarter when fixed income issuance in the US reached $2.9 trillion, or a quarter over quarter increase of 16.1%, US sustainable bond issuance in the third quarter came in at $38.3 billion, recording a modest $0.7 billion increase, or 1.9%. Year-to-date, US sustainable bond issuance reached $119.5 billion, for a year-over-year increase of $24.3 billion or 24.3%. It should be noted that SIFMA data tends to understate global sustainable bond issuance as it captures a narrower slice of the market that also includes sustainability linked bonds and notes, for example. More generally, sustainable bond data provided by different data sources can vary by significant margins. Last year, for example, UNCAD reported that global green bond issuance reached $872.2 billion while Bloomberg reported an even higher $939 billion versus $746.8 million compiled by SIFMA. More recently, according to BBVA, green, social, sustainable and SLB bond issuance through September 20, 2024, reached $698.7 billion. Of this sum, $431.0 million, or 62%, is sourced to green bonds, $108.7 billion was raised through social bonds, $133.4 billion is linked to sustainability bonds and $25.6 billion is attributable to sustainability-linked bonds. |

|

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

|

After a volatile start to September that saw the S&P 500 give up 4.2% during the first four trading days of the month, large cap stocks staged a recovery to close the month at a record level. For the month, the S&P 500 set five new closing highs and 43 closing highs year-to-date. Fueled by a sense of optimism that inflation was under control, the Federal Reserve’s 50 basis point (bps) interest rate cut will boost U.S. growth and avoid a recession, further powered at the end of the month by the announcement of a major injection of economic stimulus in China and positive expectations for corporate earnings in the third and fourth quarters, the S&P 500, which saw a broadening of stocks participating in the rally, closed the month and quarter with gains of 2.14% and 5.89%, respectively. Year-to-date, the benchmark is up by 22.08%. Other major indicators were up too. The Dow Jones Industrial Average gained 1.85%, adding 12.31% for the year and 26.3% across the trailing twelve months. At the same time, the Nasdaq 100, propelled by the performance of the Magnificent 7 that as a group, reversed the previous month’s decline, posted a gain of 2.6% in September, 20% year-to-date and a whopping 37.5% since October 1, 2023. |

Sources: Morningstar Direct, Bloomberg, MSCI, SIFMA/Dealogic and Sustainable Research and Analysis LLC