![Monitor-1-istockphoto-1437090010-612x612-3[1]](https://sustainablest.wpengine.com/wp-content/uploads/elementor/thumbs/Monitor-1-istockphoto-1437090010-612x612-31-2-r9s7e2aed1qqg9yi2cpd239lst9qqb7mxo8vlrrwks.jpg "Monitor-1-istockphoto-1437090010-612×612-3[1]")

The Bottom Line: Sustainable funds added net assets in February while green bonds flourished. Relative performance results lagged, and fund launches were missing in action.

|

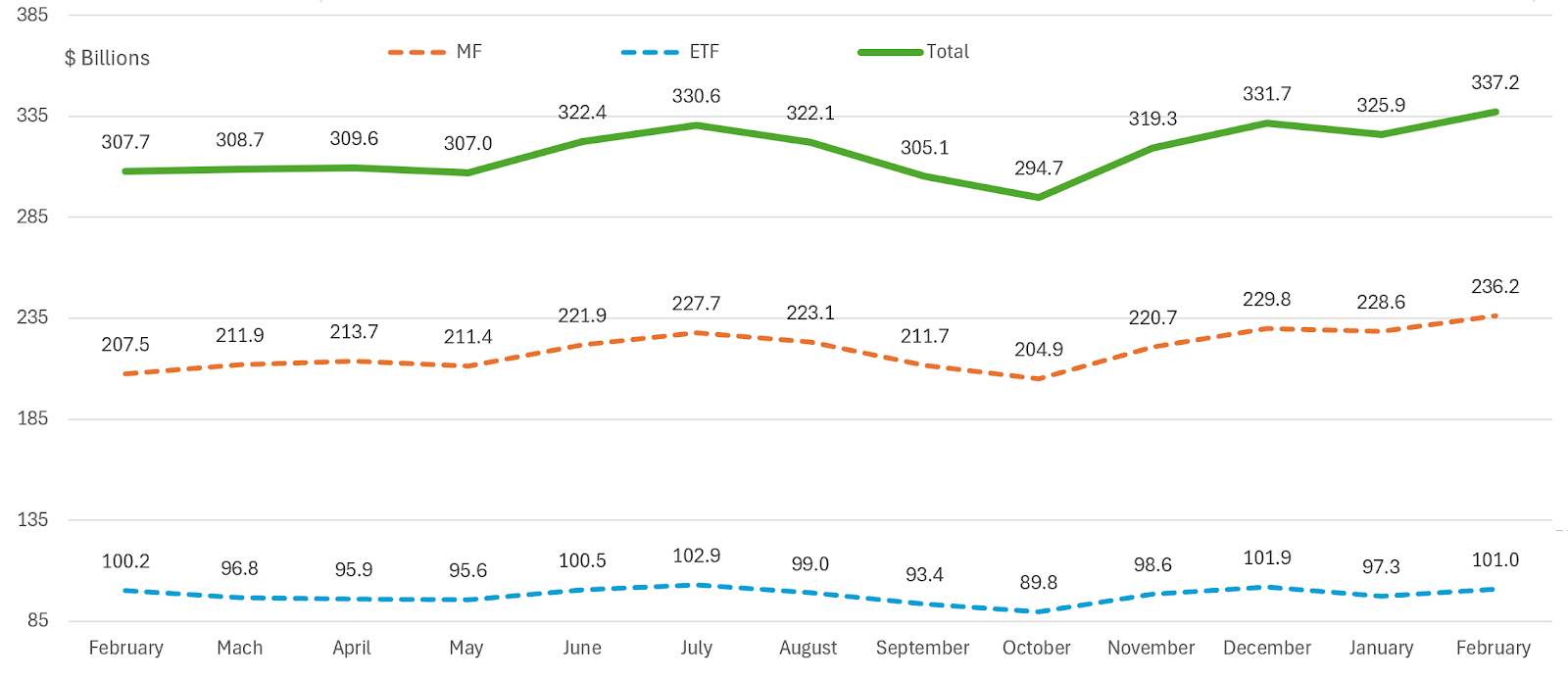

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

|

Sustainable long-term fund assets under management attributable to mutual funds and ETFs, 1,537 funds/share classes in total, based on Morningstar classifications, closed the month of February at $337.2 billion in net assets, adding $11.3 billion, or a 3.5% increase, versus a decline of $5.8 billion the previous month. This represents a month-end peak level since December 2022. Based on a simple calculation, it is estimated that sustainable funds experienced net cash inflows in February, sourced to mutual funds and ETFs. Mutual funds and ETFs added an estimated $1.3 billion and $1.2 billion, respectively, but the dominant contributor to their gains was due to capital appreciation as equity markets continued their strong start of the year while intermediate-investment grade bonds posted declines. |

|

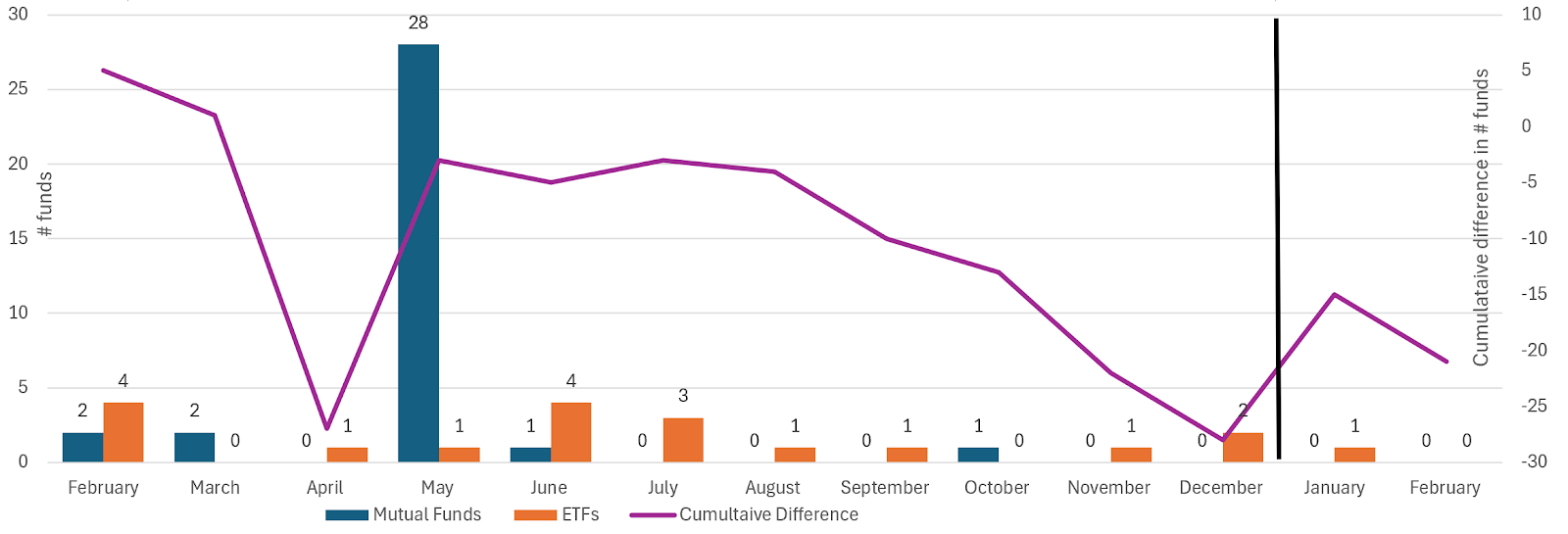

New Sustainable Fund Launches |

|

February passed without a single new sustainable mutual fund or ETF launch. By way of comparison, six new funds were listed during February 2023, including two mutual funds and four ETFs, bringing the cumulative two-month 2023 launches to 22—now 21 funds behind. Mutual fund and ETF listings started to decelerate following the launch of 29 funds in May of 2023. During the month of February there were several fund closings. Nine ETFs closed, including two with over $30 million in net assets. Notable is the closing of Wisdom Tree’s three ESG ETF offerings, with a combined total of $100 million in assets prior to closing. There were also two sustainable mutual fund closings, including one fund managed by Angel Oak that was acquired by an ETF managed by the same firm that also employs an identical ESG integration approach. |

|

Green, Social and Sustainability Bonds Issuance |

|

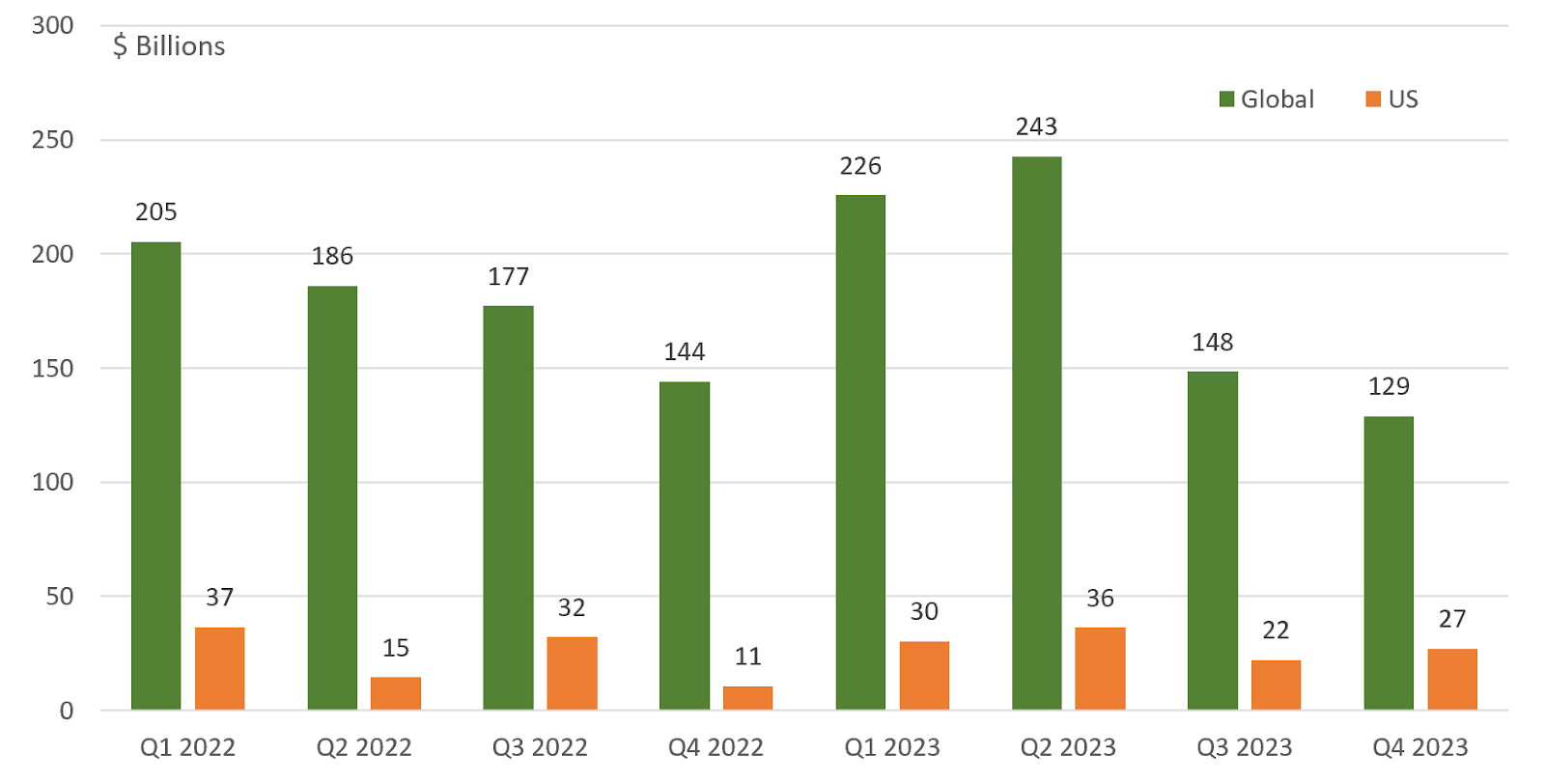

Final numbers through February are still to be determined, but according to data compiled by Bloomberg, sales of green, social, sustainability and sustainability-linked bonds reached around $90 billion in February. This, according to Bloomberg, is close to the record of roughly $91.3 billion issued in February 2023. The same source reported that sales of green bonds reached a record $54.7 billion, the most active level of issuance since the inception of the green bonds market in 2007. This follows a record January during which about $83.3 billion in green bonds were issued. As reported last month, according to data provided by SIFMA, global green, social and sustainable bond issuance in the fourth quarter of 2023 reached $128.9 billion, for a Q/Q $19.5 billion decline or 10.6%. 4Q US issuance, which declined for the second quarter in a row, dropped to $27 billion, down $1.3 billion or -4.4%. Global 2023 issuance reached $745.9 billion, for a Y/Y gain of $33.3 billion or 4.7%. Notwithstanding the deceleration in the US in the second half of 2023, total US issuance in 2023 rose to $122.0 billion, up from $93.8 billion in 2022 or a 30 Y/Y increase. It should be noted that SIFMA sustainable bonds issuance trends exclude certain types of sustainable bonds, such as sustainability-linked bonds and notes. According to data published by another source, for example Bank of America, total global sustainable bond issuance in 2023 reached $828 billion, for a Y/Y 7% gain. Of this sum, green bonds account for 59% of the total, or $489 billion, up 12% Y/Y. Some other data sources have arrived at even higher numbers for global issuances. |

|

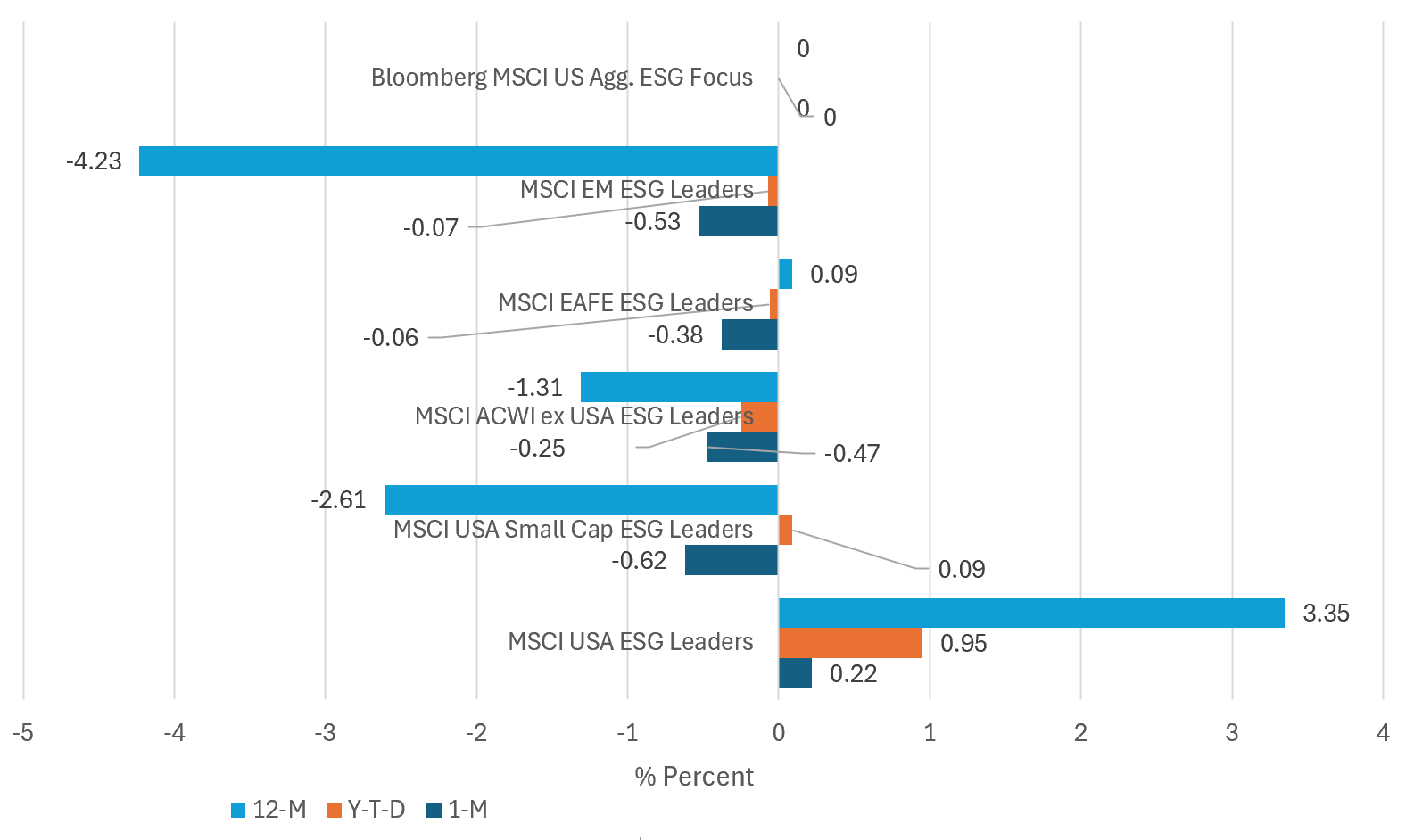

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

|

Equity markets continued their strong start to the year in February, with the S&P 500 Index recording its fourth consecutive monthly gain. The index closed above 5000 for the first time and produced a total return of 5.3%, expanding January’s gain of 1.7% to reach an increase of 7.1% since the start of the year. Non-US stocks, including large and mid-cap companies representing developed and emerging market countries, were up 2.53% according to the MSCI ACWI ex USA Index. At the same time, the US bond market retreated as concerns that the Federal Reserve may be less inclined to lower interest rates amid economic strength led to rate reduction expectations being adjusted from March to June. Bonds declined 1.41% in February and 1.68% year-to-date, per the Bloomberg US Aggregate Bond Index. Reversing January’s results, during which a selection of six US and international equity ESG indices and one fixed income benchmark calculated by MSCI either matched or outperformed their conventional counterparts, only two of six ESG indices either matched or outperformed their conventional counterparts in February. These include the MSCI USA ESG Leaders Index and the Bloomberg MSCI US Aggregate ESG Focused Index that outperformed or matched their conventional counterparts by 22 bps and 0 bps, respectively. Emphasizing companies that are assigned high environmental, social and governance ratings by MSCI relative to their sector peers, the year-to-date results of these selected indices are now mixed—with three domestic tracking equity and fixed income ESG indices outperforming while the three international ESG indices are lagging. Similar outcomes are applicable to the intermediate-term time horizons of three and five years, but with shifting geographic patterns of outperformance/underperformance. |

Sources: Morningstar Direct, Bloomberg, MSCI, Bank of America and Sustainable Research and Analysis.