![Monitor-1-istockphoto-1437090010-612x612-3[1]](https://sustainablest.wpengine.com/wp-content/uploads/elementor/thumbs/Monitor-1-istockphoto-1437090010-612x612-31-2-r9s7e2aed1qqg9yi2cpd239lst9qqb7mxo8vlrrwks.jpg "Monitor-1-istockphoto-1437090010-612×612-3[1]")

The Bottom Line: Sustainable fund assets expanded modestly, sustainable bond issuance remains strong, ESG relative performance results were positive, but fund launches were still anemic.

|

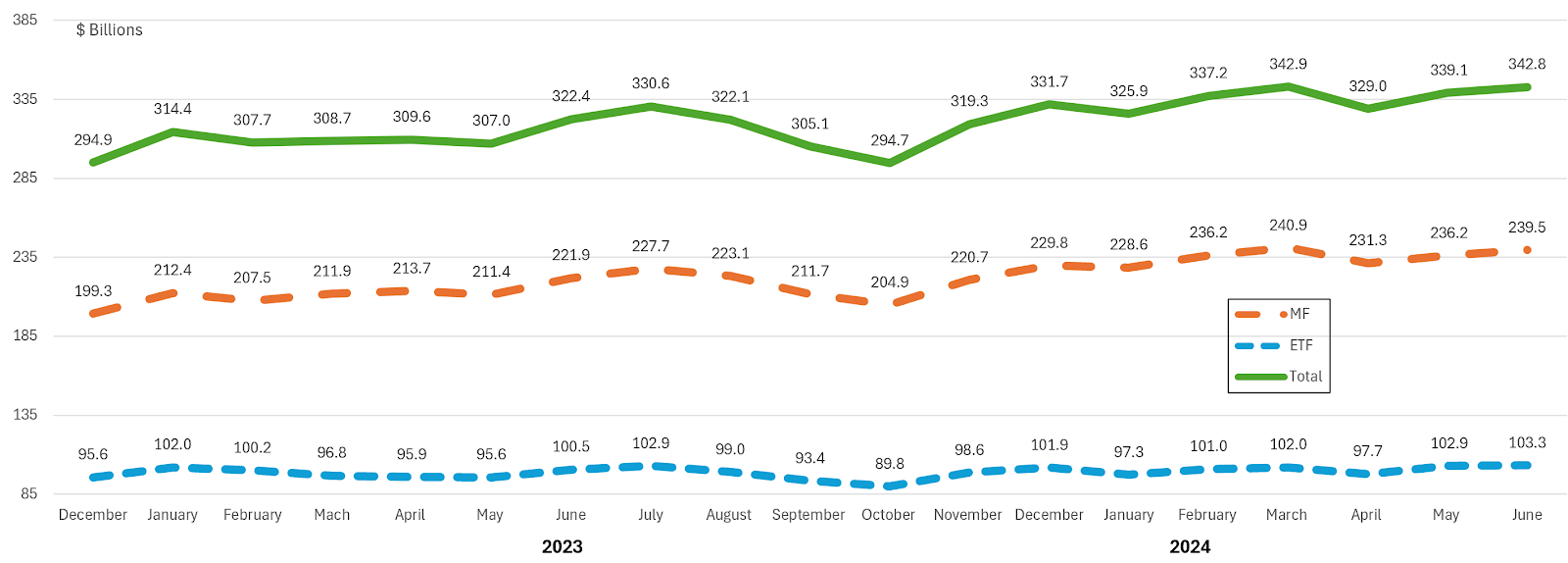

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

|

Focused sustainable long-term fund assets under management attributable to mutual funds and ETFs (excluding money market funds), 1,454 funds/share classes in total, based on Morningstar classifications, closed the month of June at $342.8 billion in net assets. This represents a modest $3.7 billion net pick up in assets, or an increase of 1%, versus $339.1 billion the previous month and brings the combined total of focused sustainable mutual funds and ETFs to within a hair breadth away of the month-end high point for assets reached this year in March. Since then, net assets have been flat. Based on a simple calculation that reflects the average June total return gains recorded by long-term mutual funds at 0.8% and -1.23% by ETFs, it is estimated that sustainable funds experienced narrow cash inflows in the amount of $3.1 billion. Since the start of the year, focused sustainable mutual funds and ETFs have added a combined net of $11.1 billion in assets, 88% of which is attributable to mutual funds. |

|

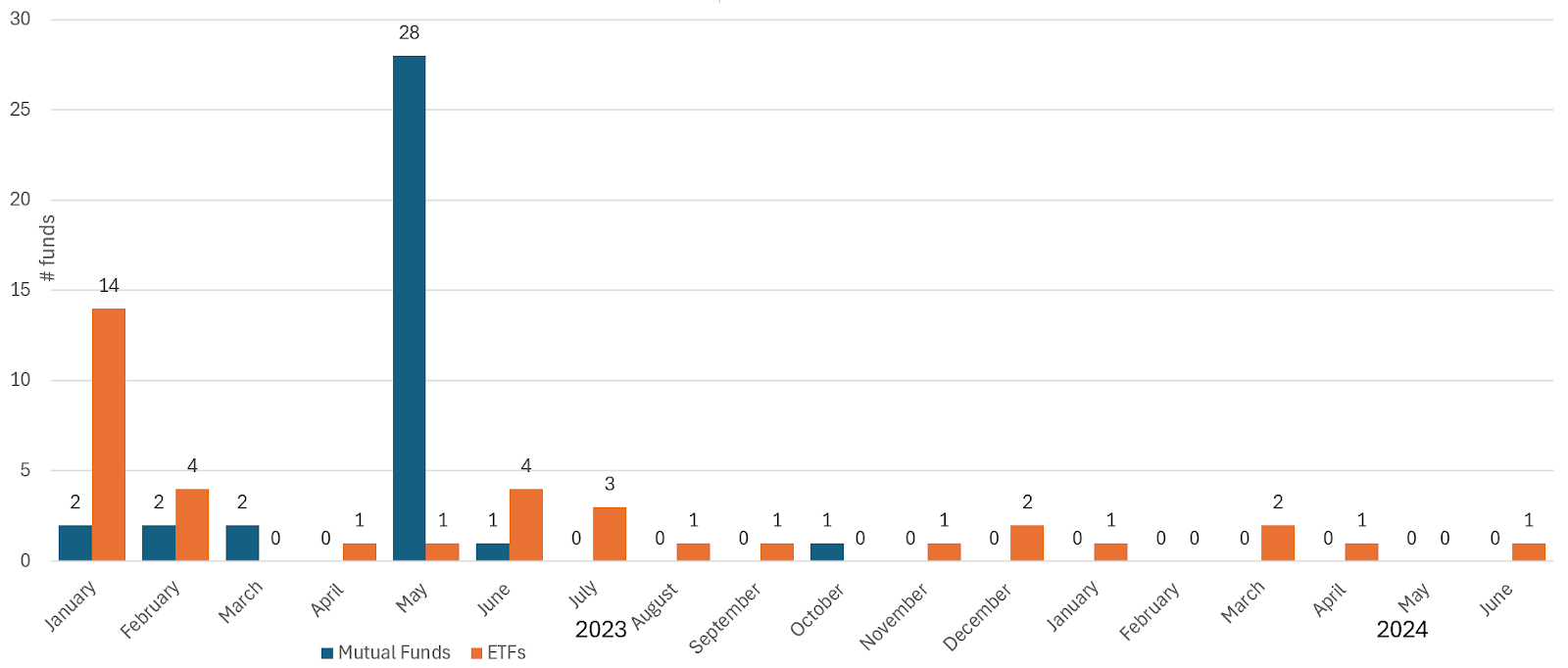

New Sustainable Fund Launches |

|

Even as one ETF was launched in June 2024, versus zero fund launches last month, it’s fair to say that the drought in sustainable fund launches continued through the end of June. During the six-month interval, only five new funds were introduced, all ETFs. This stands in sharp contrast to the 59 funds that were launched during the comparable period in 2023. At the same time, one ETN, one ETF and two mutual funds were shuttered. The new ETF is the Invesco MSCI Global Climate 500 ETF, making its debut with $1.6 billion in assets. The fund intends to track the performance of approximately 500 stocks included in the MSCI ACWI ex 6 Countries Index that meet certain environmental and climate criteria relative to their peers, including their own reductions in carbon and greenhouse gas emissions. The scarcity in sustainable fund launches, starting after May of last year, may be attributable to the fact that anti-ESG movement in the US had gained momentum in the second quarter of 2023 and fund companies may have opted to lower their profile by curtailing focused fund offerings. At the same time, commitments to ESG integration do not appear to have subsided, based on reporting by the largest fund companies. |

|

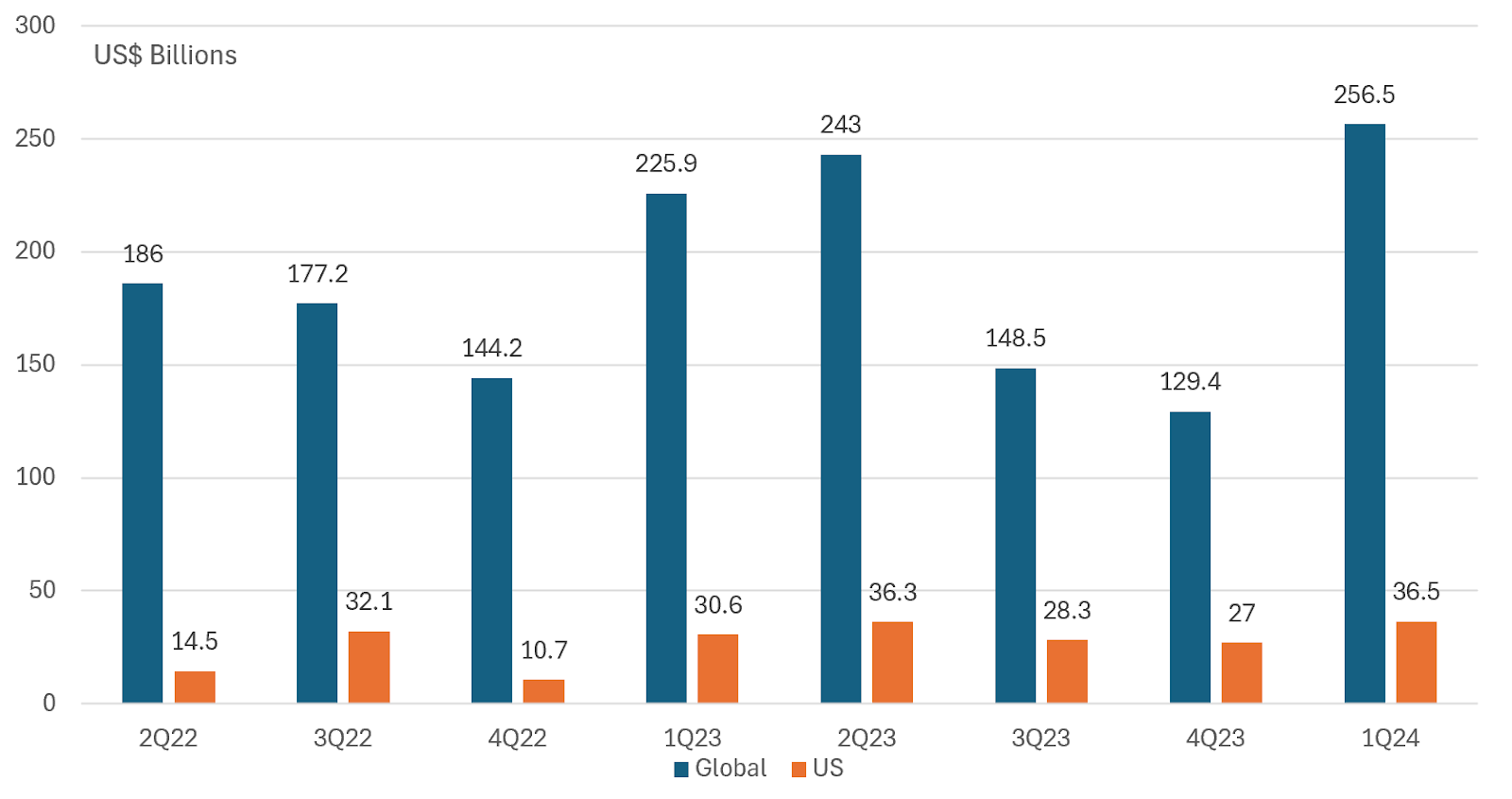

Green, Social and Sustainability Bonds Issuance |

|

While second quarter data is not yet available, green debt issuance globally is running at a fast pace and projections for green, social and sustainable bond (GSS) issuance indicate that global issuance could reach and perhaps exceed the USD 1 trillion-dollar mark. Moody’s, for example, projects that green, social and sustainable bond issuance could reach US$ 950 billion in 2024, slightly higher than 2023’s US$ 946 billion, while S&P’s forecasts indicate that issuance could rise to above the US$ 1 trillion mark and perhaps equal or exceed the record level registered in 2021. According to Morgan Stanley issuance will be fueled by the perception that climate is the biggest single existential threat of our time and issuers are focusing more narrowly on their climate and transition objectives, particularly as the year 2030 gets closer. Another factor, according to Morgan Stanley, is the tremendous demand for power because of the AI boom. This phenomenon is putting increased demand on the need for additional power sources, renewable or otherwise, including alternative power sources, that will require significant investments to meet the emerging demand. Other drivers include the increasing role of sovereign issuers, both in emerging and developed markets. As of April 2024, 53 sovereign issuers have issued GSS-labeled bonds totaling $540 billion. Beyond the main players, countries such as Chile, Indonesia, Japan, Iceland and Australia have issued green bonds in 2024. In addition, voluntary frameworks, such as the International Capital Market Association (ICMA) introduced new criteria and further guidelines to support the green, social, sustainability, and sustainability-linked bond principles as well as the implementation of regulations, such as the EU Bond Standard, that attempts to establish clarity and comparability for sustainable bonds across Europe that’s going into effect starting on December 21, 2024. On the positive side, such standards should bring about a higher level of confidence in such instruments to investors. While other reports covering sustainable debt volumes in the first quarter 2024 quote even higher volumes, the latest available data according to SIFMA show that global green, social and sustainable bond issuance in the first quarter of 2024 rose to $256.5 billion, for a Q/Q $127.9 billion increase or nearly doubling the issuance level recorded during the previous quarter. January was the strongest month, during which $123.2 billion in green, social and sustainability bonds were issued—led by green bonds over the quarter (but not in the US where sustainability bonds dominated). Issuance volumes moderated in February and March. U.S. issuance gained too, reaching $36.5 million for a Q/Q gain of 35% and exceeding the previous 2Q 2023 quarterly high mark since early 2022. This came on the heels of strong Q1 aggregate issuance levels for bonds in the US that saw an increase of $2.5 trillion for a 26% gain. |

|

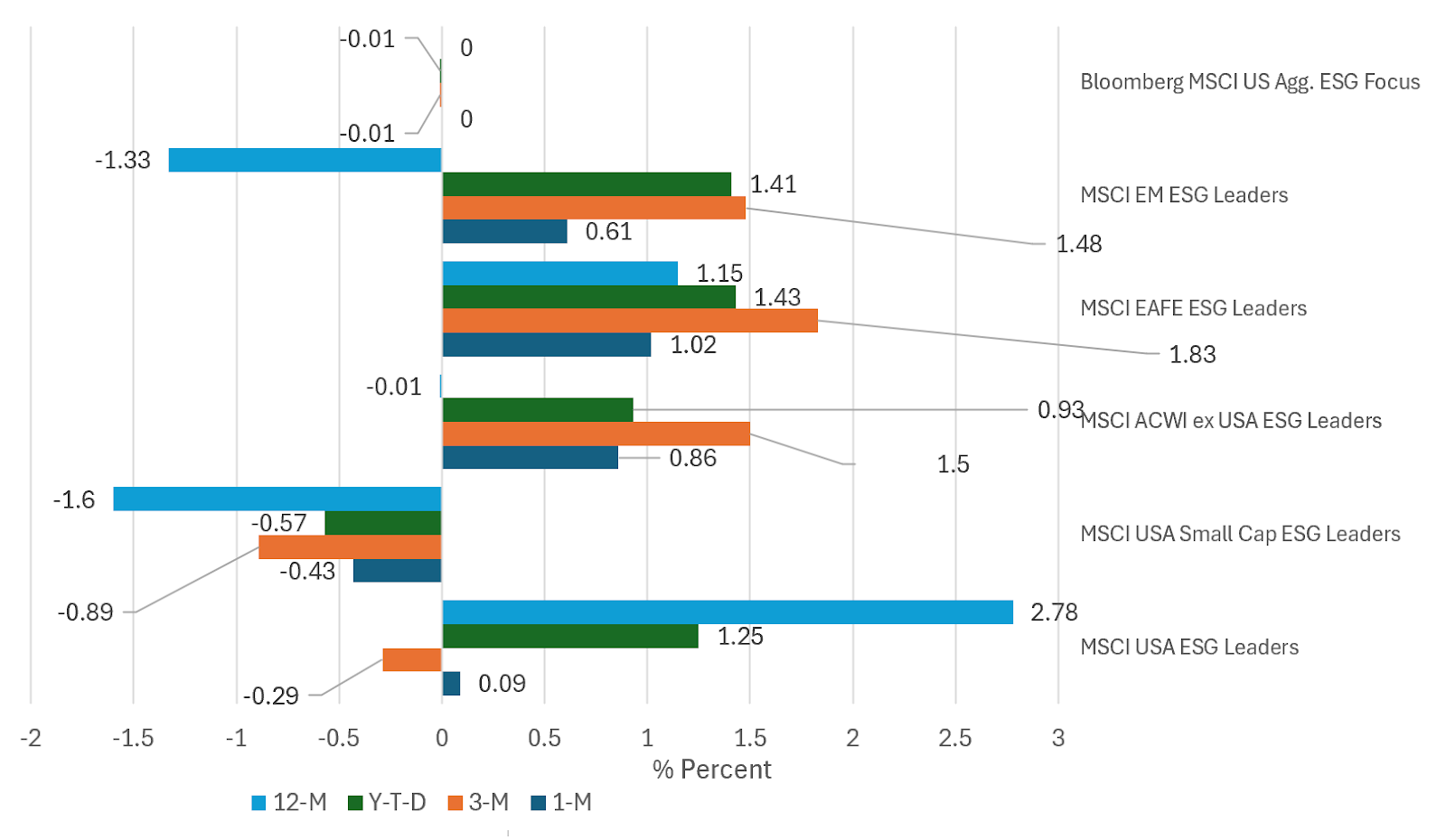

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

|

Fueled by enthusiasm for AI and expected interest-rate cuts before the end of the year in the light of softening economic data, the S&P 500 continued to register gains in June. After recording a 5% total return in May, the index posted seven new closing highs in June and ended the month up 3.6%. This was the benchmark’s fifth monthly gain this year, for a year-to-date increase of 15.9% and a trailing twelve-month return of 24.6%. At the same time, the S&P 500 ESG index, designed to meet S&P’s sustainability criteria while maintaining similar overall industry group weights as the S&P 500, was up 3.4% in June. While trailing in June, the ESG index is ahead of the S&P 500 with returns of 15.8% year-to-date and 25.1% over the trailing twelve-months. The performance of the conventional large cap index and ESG version have been driven by a small number of growth-oriented technology companies that now dominate the index. The same companies drove the performance of the S&P 500 Growth Index, up 6.98% in June, versus the S&P 500 Value Index that sustained a narrow -0.65% decline. This dynamic also propelled large cap conventional and sustainable growth funds to achieve top results in June. At the same time, small companies experienced another challenging month, with the Russell 2000 dropping 0.93%, after dropping around 1% in May and an even lower -1.69% posted by the Russell 2000 Value Index. On the bonds side, the Bloomberg Aggregate US Bond Index posted a slight 0.95% gain in June and a positive 2.6% increase over the trailing twelve months. During the month, the FOMC met and as expected, kept interest rates unchanged. The 10-year U.S. Treasury Bond closed at a yield of 4.36%, down from the prior month’s 4.51% Overseas, strong performance in emerging markets pushed the MSCI Emerging Markets Index higher by 3.94% in June while the MSCI ACWI, ex USA Index and MSCI EAFE Index gave up 0.10% and -1.61%, respectively. Against this backdrop, based on a selection of five US and international equity ESG Leaders indices and one fixed income benchmark, all constructed by MSCI around ESG screening and exclusionary criteria, four of the six ESG indices recorded positive relative performance results in June while only two beat their conventional counterparts over the trailing twelve months. Total return margins of outperformance in June ranged from a low of 9 bps to a high of 1.02%. At the same time, the MSCI USA Small Cap ESG Leaders Index lagged in June while the Bloomberg MSCI US Aggregate ESG Focus Index came in even with its conventional counterpart. Over the intermediate and long-term time frames, based on three-, five- and ten-year time periods, the results remain mixed but improve over longer time periods. Over the trailing three-year time horizon, only two of the six benchmarks, or 33%, outperform but this ratio improves to four out of five, or 80%, over the trailing ten-year time interval. |

Sources: Morningstar Direct, Bloomberg, MSCI, SIFMA/Dealogic and Sustainable Research and Analysis LLC