![Monitor-1-istockphoto-1437090010-612x612-3[1]](https://sustainablest.wpengine.com/wp-content/uploads/elementor/thumbs/Monitor-1-istockphoto-1437090010-612x612-31-1-r9s7e2aed1qqg9yi2cpd239lst9qqb7mxo8vlrrwks.jpg "Monitor-1-istockphoto-1437090010-612×612-3[1]")

The Bottom Line: Long-term fund assets gained due to market appreciation, new fund formations decelerated, sustainable bonds and the performance of selected ESG indices lagged.

|

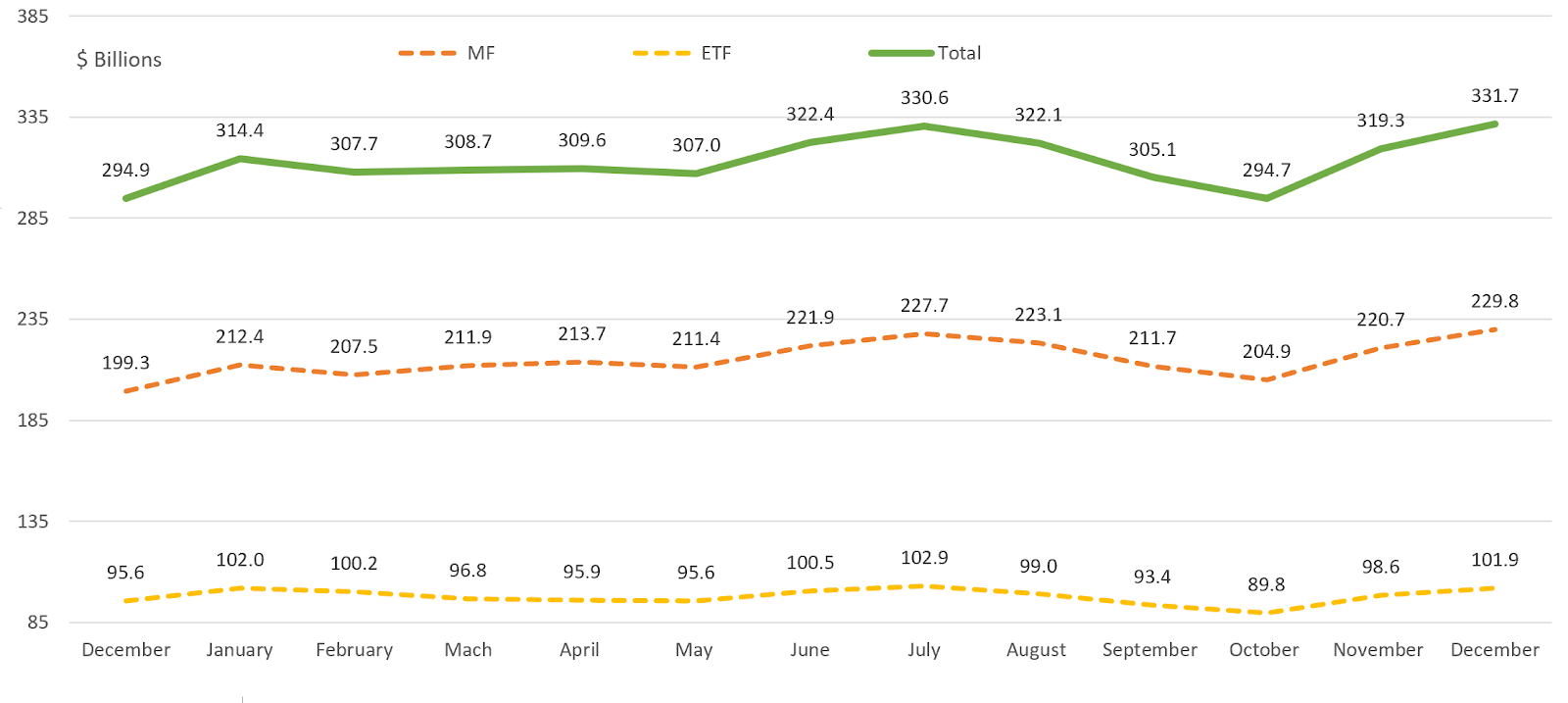

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

|

Sustainable long-term fund assets under management attributable to mutual funds and ETFs added $12.4 billion, or 4.2%, in net assets in December, ending the year with $331.7 billion. This was the highest month-end level achieved in 2023, reflecting a $36.8 billion net increase since the start of the year due entirely to strong market gains that were bolstered by the fourth quarter results achieved in both the stock and bond markets. ETF assets ended the year still slightly below the month-end high reached in July, but up $6.3 billion over the 12-month interval. Mutual funds, which make up 69% of sustainable fund assets, reached a month-end high of $229.8 billion at the end of December with the addition of $30.5 billion (net) over the course of the year. Note: Revised data to reflect latest updates, excluding sustainable money market funds. |

|

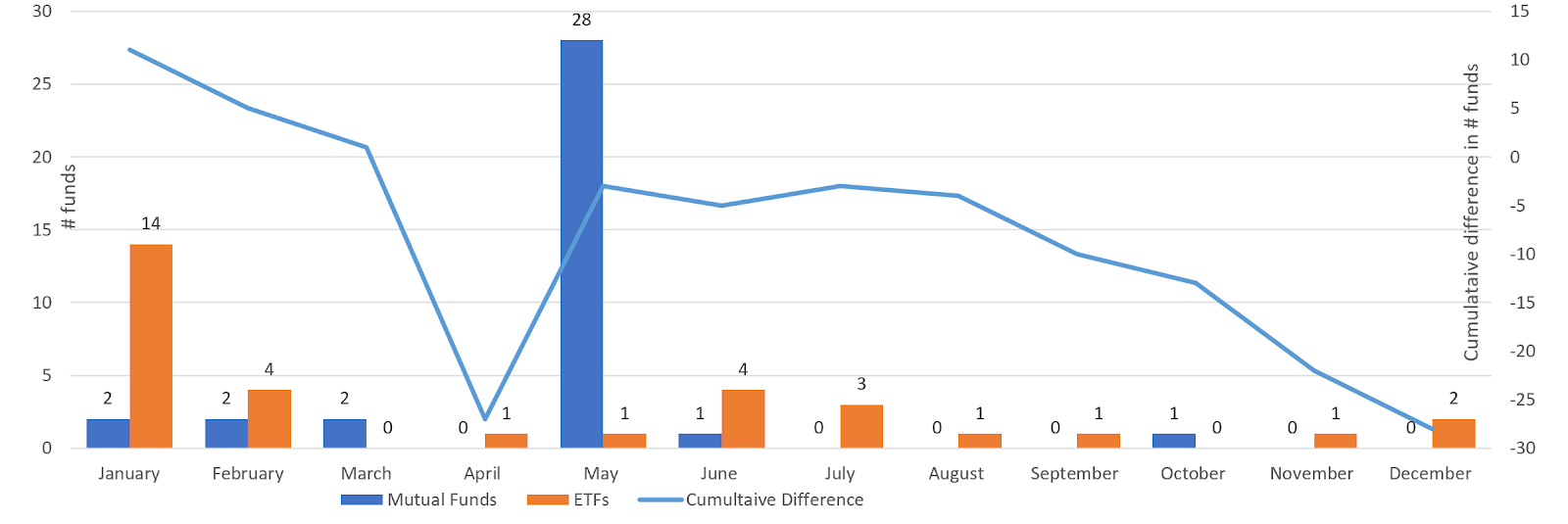

New Sustainable Fund Launches |

|

Two new investment funds were listed in December, consisting of two new ETFs and zero mutual funds, bringing the year-to-date total ETF launches to 32 and mutual fund launches (excluding share classes) to 36, for a combined 2023 total of 68 investment funds. There were three ETF closures in December and, excluding share classes, zero closings of mutual funds. Mutual fund and ETF listings decelerated in 2023 relative to 2022 with 28 fewer fund launches. |

|

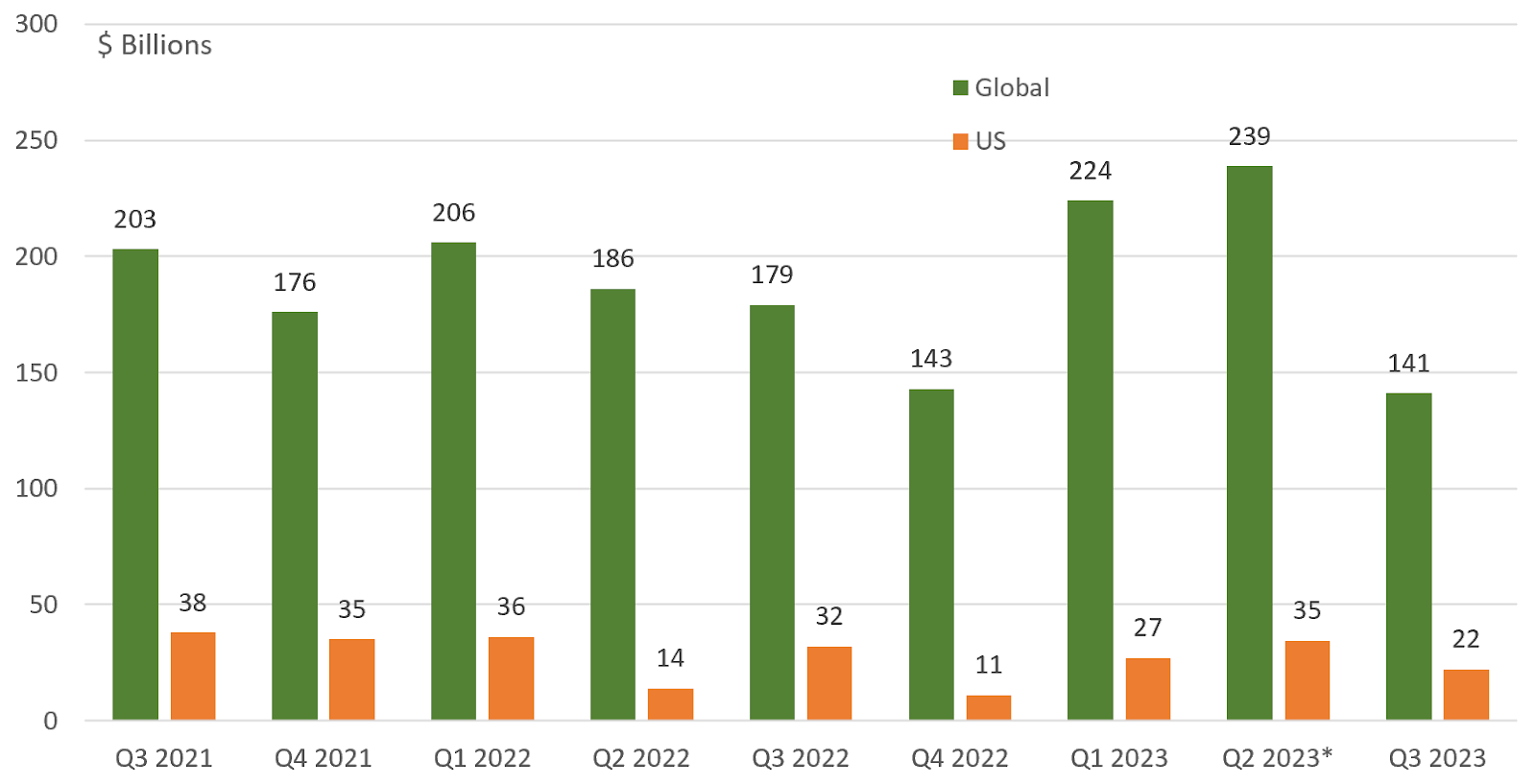

Green, Social and Sustainability Bonds Issuance |

|

Based on preliminary data, green, social, sustainability and sustainability-linked bond issuance through the end of 2023 reached $828 billion, reflecting an increase relative to 2022 but still trailing 2021 in terms of volume. Sovereign bonds experienced gains, mainly from green bonds which also experienced an increase to $489 billion. Green bonds were 59% of labeled issuance in 2023. Issuance in the US fell from $52 billion in 2022 to $36 billion in 2023 and sustainability linked bonds dropped from $69 billion to $60 billion. |

|

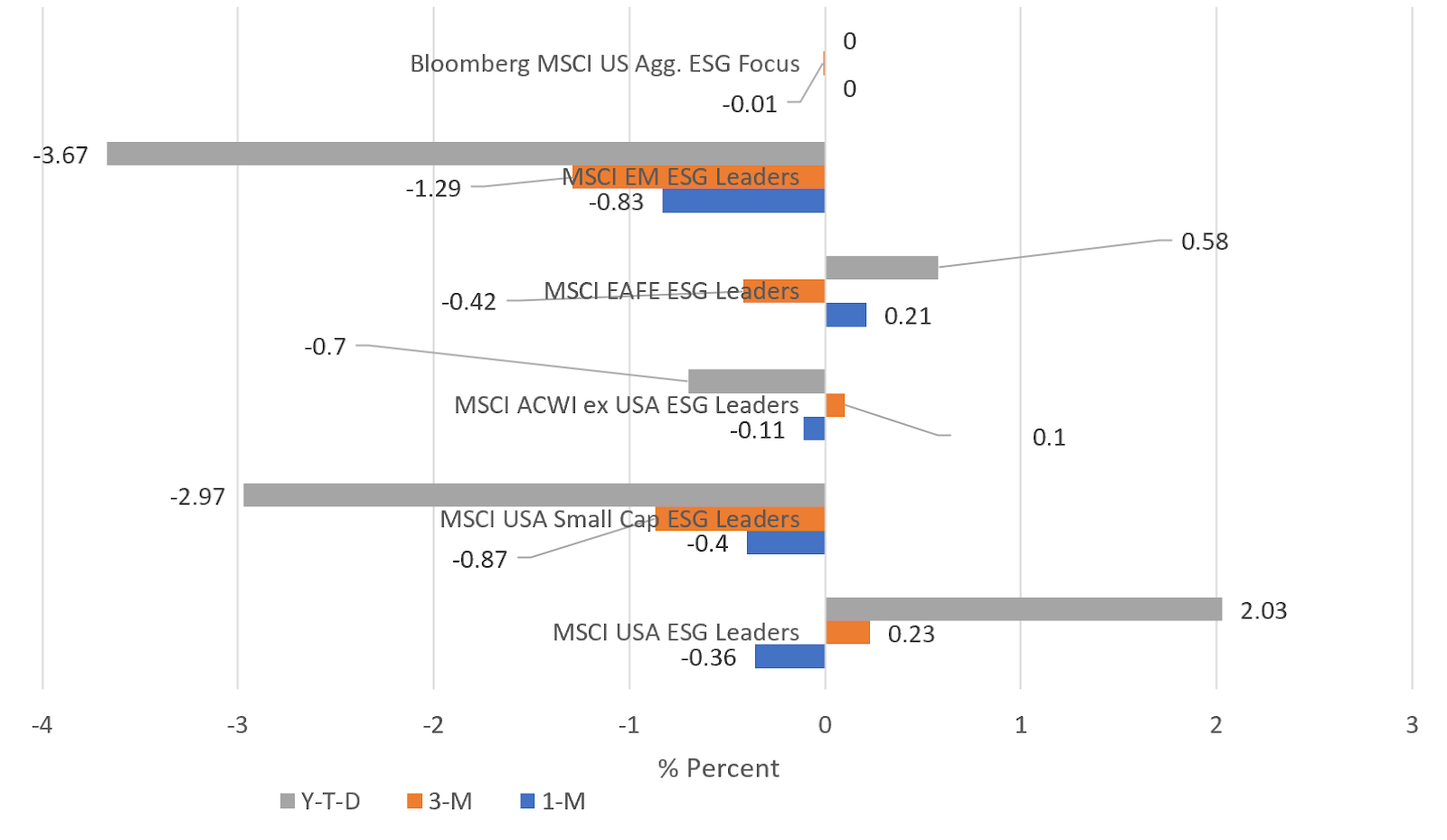

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

|

Markets continued to rally in December, fueled by the combination of a strong economy and reduced concerns of a looming recession, better-than-expected corporate earnings, lower inflation and an apparent end to the Federal Reserve’s interest rate hikes that were expected to lead to multiple Fed rate cuts in 2024. Stocks, as measured by the S&P 500, posted a gain of 4.5% in December and a full year increase of 26.3%. At the same time, credit markets continued to rebound, gaining 3.8% in December and 5.53% for the full calendar year. Against this backdrop, mutual funds and ETFs gained an average of 5.1% in December and 13.5% over 2023. At the same time, only one of six selected ESG indices outperformed their conventional counterparts in December while four of six indices trailed behind while one ESG index matched the performance of its conventional counterpart. Over weightings/under weightings (>1%) in some sectors that may have contributed positively to performance were offset by the performance of individual stocks based on their respective weights. For the calendar year period, two of the six selected ESG indices outperformed their conventional counterparts. |

Sources: Morningstar Direct, Bloomberg, MSCI, Bank of America and Sustainable Research and Analysis.