![Monitor-1-istockphoto-1437090010-612x612-3[1]](https://sustainablest.wpengine.com/wp-content/uploads/elementor/thumbs/Monitor-1-istockphoto-1437090010-612x612-31-2-r9s7e2aed1qqg9yi2cpd239lst9qqb7mxo8vlrrwks.jpg "Monitor-1-istockphoto-1437090010-612×612-3[1]")

The Bottom Line: Sustainable funds gave up assets in March while green bonds flourished. Relative performance results lagged, and fund launches continue to cool off.

|

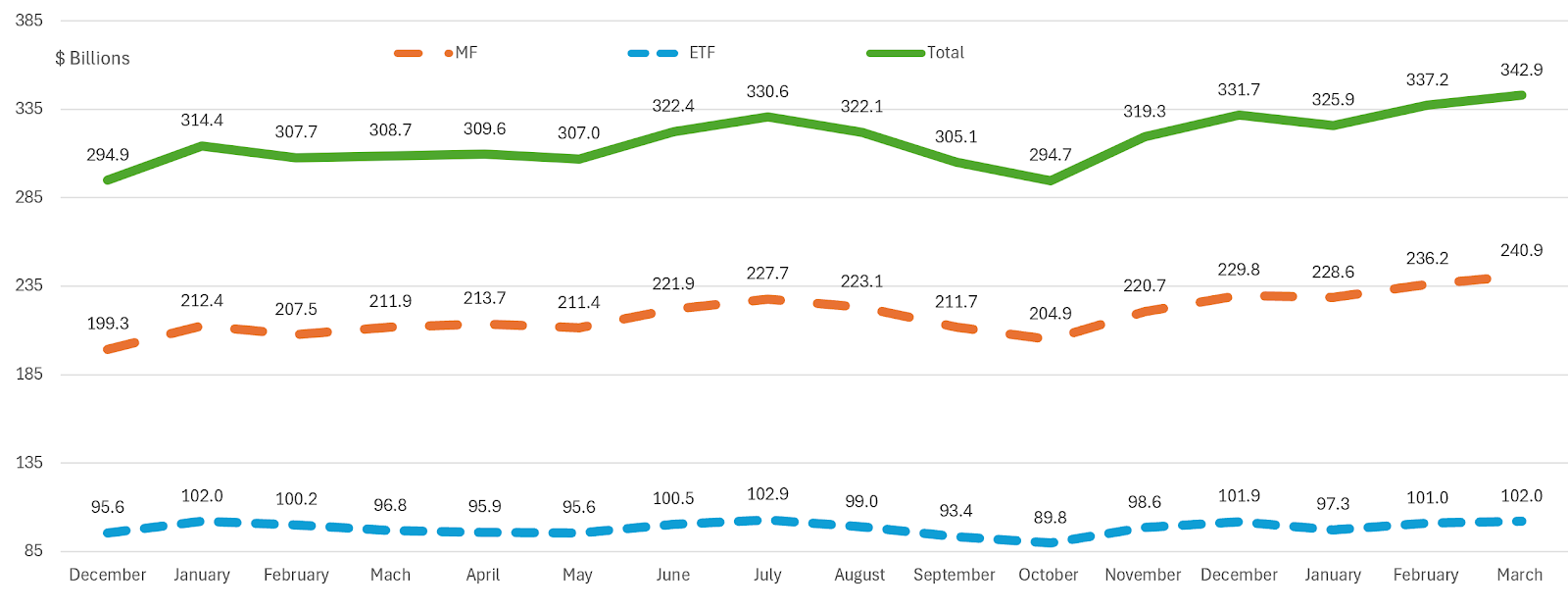

Long-Term Net Assets: Sustainable Mutual Funds and ETFs |

|

Sustainable long-term fund assets under management attributable to mutual funds and ETFs, 1,527 funds/share classes in total, based on Morningstar classifications, closed the month of March at $342.9 billion in net assets. This represents a month-over-month increase of $5.7 billion, or 2.4%, or just about half the gain realized in February when assets increased by $11.3 billion. Based on a simple calculation predicated on the average 2.4% March total return performance results achieved by long-term fund, it is estimated that sustainable funds experienced net cash outflows of $2.4 billion. Since the start of the year, sustainable mutual funds and ETFs added a net of $11.3 billion, for a three-month gain of 3.4%. While the ETF segment has still not exceeded the month-end high level recorded at the end of July 2023, mutual funds have managed to eclipse the previous month-end high of $330.6 billion as of the same month. |

|

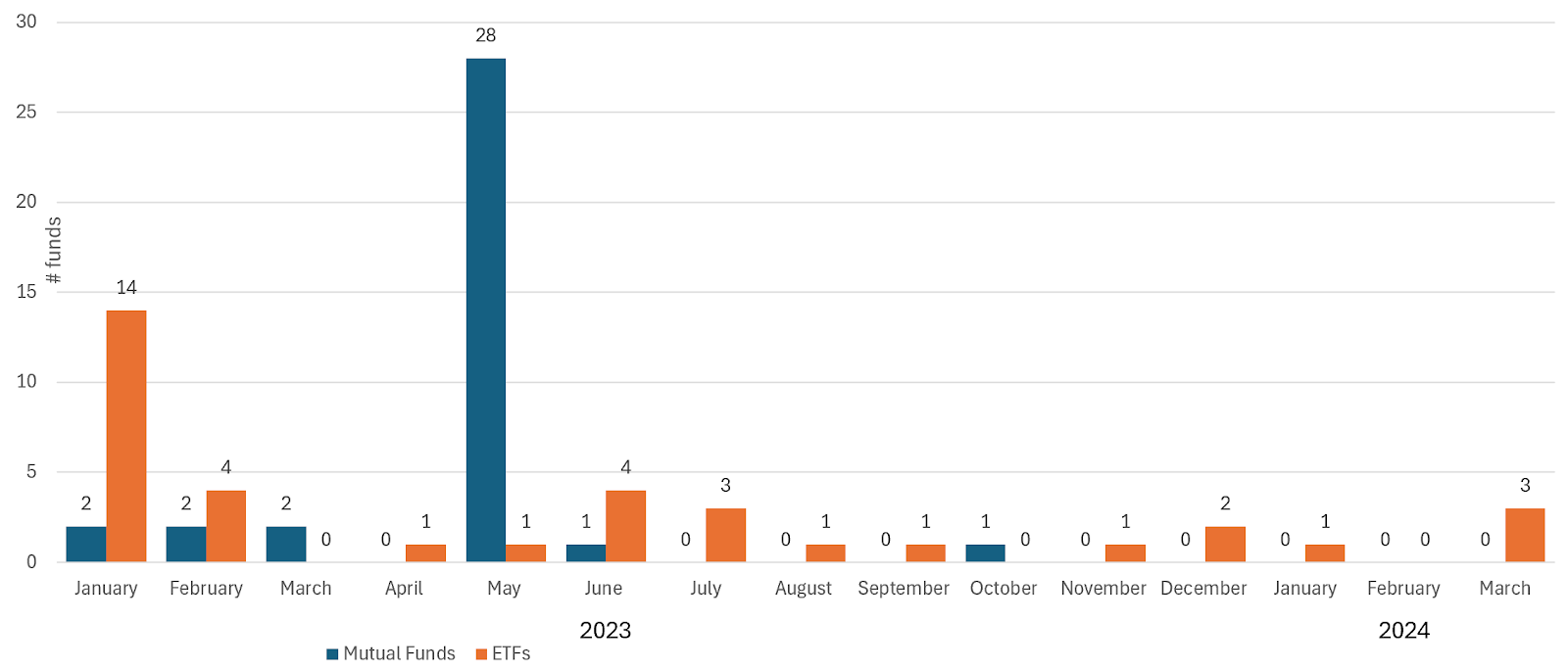

New Sustainable Fund Launches |

|

Reflecting a cooling off in sustainable fund introductions, only three new sustainable funds were launched in March of this year. All are ETFs, including the actively managed Nuveen Sustainable Core ETF (NSCR) and the index tracking iShares Energy Storage & Materials ETF (IBAT) as well as Inspire 500 ETF (PTL). Alongside, there were no new mutual fund introductions in March. Through the end of the first quarter, a total of only four sustainable funds have been launched, all four ETFs. There were no new sustainable mutual fund listings so far this year. By way of comparisons, 18 sustainable ETFs were launched in Q1 2023 along with six sustainable mutual funds, for a total of 24 funds (excluding new share classes). The number of sustainable fund launches also trails when compared to the number of conventional funds that started operations in the first quarter of this year. |

|

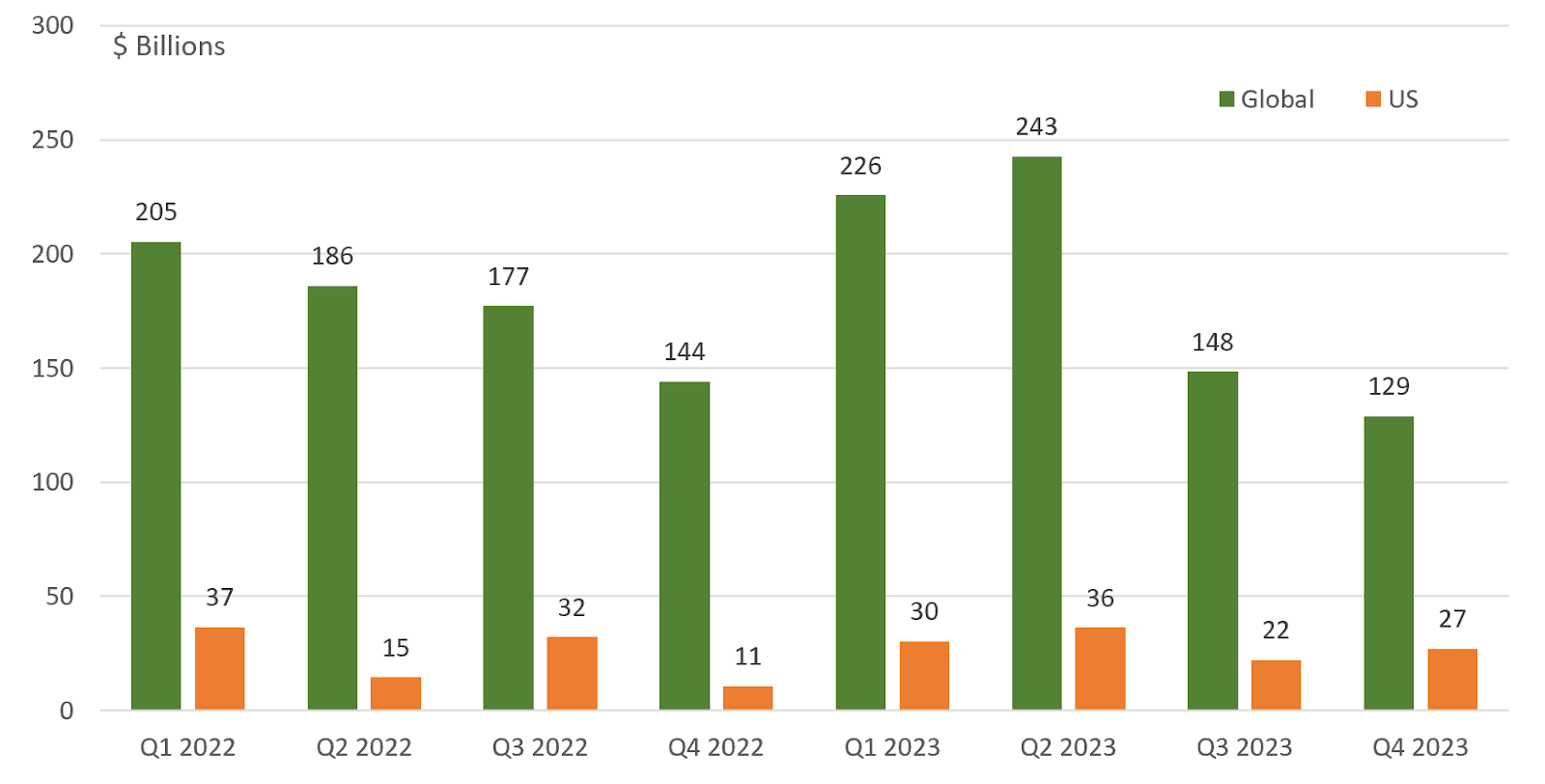

Green, Social and Sustainability Bonds Issuance |

|

According to Bloomberg News, issuance of new green bonds, the largest category of sustainable debt by volume, reached $187.7 billion in the first quarter. Record sales in January and February boosted the quarterly figure, “driven by governments taking advantage of the sanguine credit markets to bring large deals.” At the same time, sales of sustainability bonds used to fund both green and social projects totaled $64.3 billion in the same period. These data points are expected to be confirmed later in the month. As reported in February, according to data provided by SIFMA, global green, social and sustainable bond issuance in the fourth quarter of 2023 reached $128.9 billion, for a Q/Q $19.5 billion decline or 10.6%. 4Q US issuance, which declined for the second quarter in a row, dropped to $27 billion, down $1.3 billion or -4.4%. Global 2023 issuance reached $745.9 billion, for a Y/Y gain of $33.3 billion or 4.7%. Notwithstanding the deceleration in the US in the second half of 2023, total US issuance in 2023 rose to $122.0 billion, up from $93.8 billion in 2022 or a 30 Y/Y increase. It should be noted that SIFMA sustainable bonds issuance trends exclude certain types of sustainable bonds, such as sustainability-linked bonds and notes. According to data published by another source, for example Bank of America, total global sustainable bond issuance in 2023 reached $828 billion, for a Y/Y 7% gain. Of this sum, green bonds account for 59% of the total, or $489 billion, up 12% Y/Y. Some other data sources have arrived at even higher numbers for global issuances. |

|

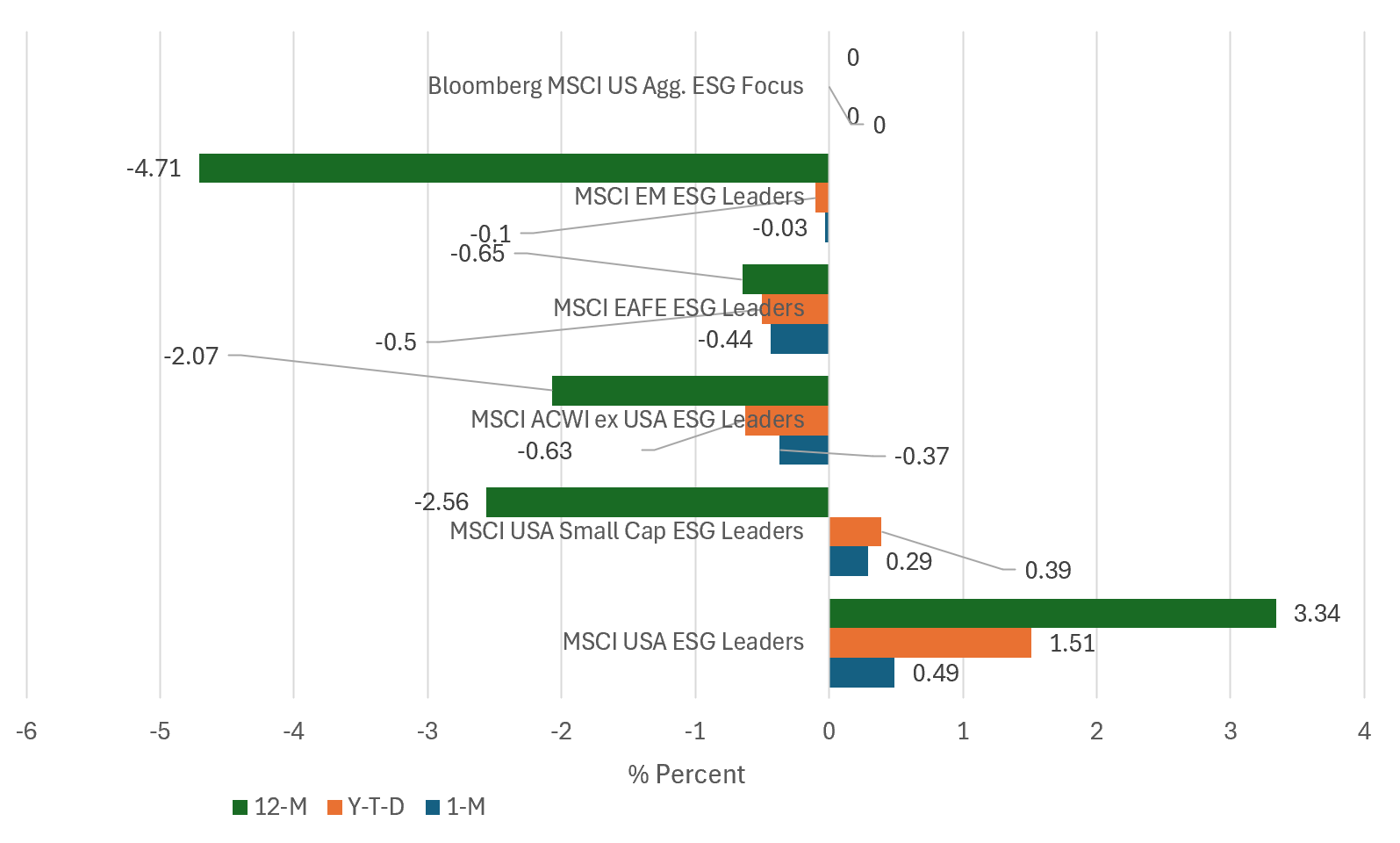

Short-Term Relative Performance: Selected ESG Indices vs. Conventional Indices |

|

Investor optimism about the U.S. economy, earnings growth, enthusiasm about artificial intelligence (AI) opportunities, and, although these had begun to moderate, expectations for interest-rate cuts later this year, powered the broad stock market higher to end the month and the quarter at a new all-time high of the year. The S&P 500 added 3.2% in March and advanced 10.6% in the quarter to cap off its best three-month interval since 2019. The Nasdaq 100 was up 1.23%, 8.72% for the quarter and 39.65% over the trailing twelve-months, as the new Gang of Four stocks, including Nvidia, Microsoft, Meta Platforms (META) and Amazon.com recorded strong gains. Small cap stocks, as measured by the Russell 2000, exceeded the performance of large cap stocks with a gain of 3.58% but continue to trail large caps over the quarter and trailing twelve months at 5.18% and 19.7%, respectively. Outside the US, emerging markets outperformed developed and emerging markets, combined, adding 3.3% versus 3.1%. The Bloomberg US Aggregate Bond Index squeezed out a small gain, adding 0.92% in March and ending in the red for the quarter with a drop of 0.78%. Against this backdrop, sustainable mutual funds and ETFs combined, a total of 1,521 funds and share classes at the end of March, gained an average of 2.4% in March, 4.4% over the first quarter of the year and 13.0% over the trailing twelve months. US stock funds gained an average of 3.3%, taxable bond funds were up 0.91% and international equity funds recorded a gain of 2.7%. At the same time, the selection of five US and international equity ESG indices and one fixed income benchmark, calculated by MSCI, were dominated by benchmarks that either matched or underperformed their conventional counterparts. Two of six ESG indices outperformed their conventional counterparts. These include the MSCI USA ESG Leaders Index and the MSCI USA Small Cap ESG Leaders Index that outperformed their conventional counterparts in March by 49 and 29 basis points, respectively. Except for the small cap index over the trailing twelve months, the two indices also outperformed their conventional counterparts on a year-to-date basis and trailing twelve months. In contrast, the three selected non-US indices each lagged their conventional counterparts in March by a range between 3 and 44 basis points. The same indices underperformed their conventional counterparts over the trailing three- and twelve-month intervals. Concurrently, the Bloomberg Barclays MSCI US Aggregate ESG Focus Index matched the performance of its counterpart conventional benchmark. Over the intermediate-to-long term, intervals of three, five and ten years, relative performance results tend to be mixed. |

Sources: Morningstar Direct, Bloomberg, MSCI, Bank of America and Sustainable Research and Analysis.