Sustainable Bottom Line: The ten largest focused sustainable long-term funds at YE 2025 include four leading fund candidates for consideration in core positions within portfolios.

Notes of Explanation: L-T=long-term funds (excluding money market funds); *=fund rated A (refer to notes); in the case of mutual funds, fund performance results apply to the largest share class. Sources: Morningstar, Sustainable Research and Analysis LLC.

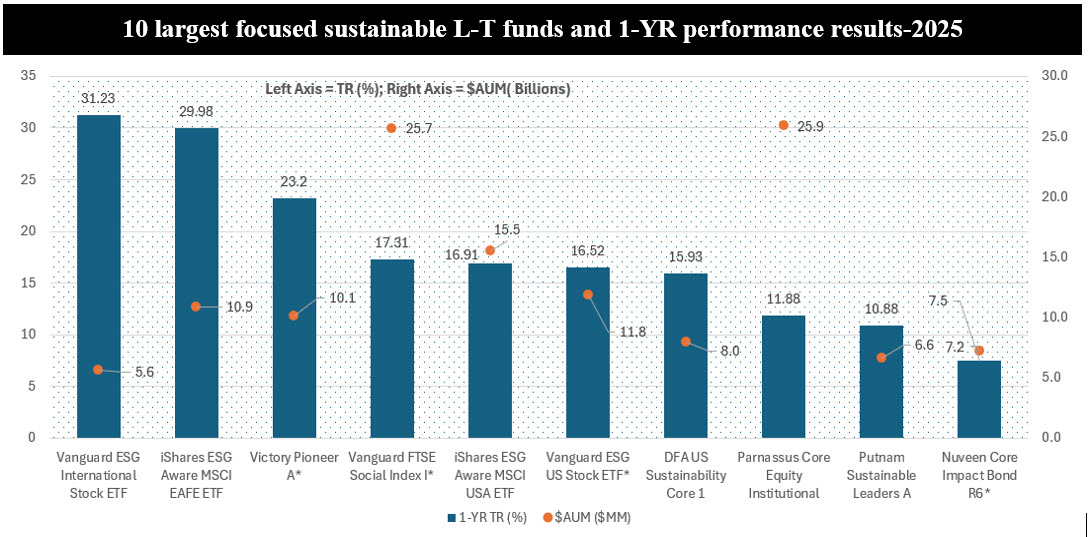

Summary:

• The ten largest focused sustainable long-term funds, including mutual funds and ETFs, ended 2025 with $127.3 billion in assets under management, accounting for 34% of the segment’s $374.6 billion in assets as of the same date. This was a slight drop from 34.7% at the end of 2024.

• Consisting of US and international equity funds as well as one core bond fund, these ten investment funds posted strong returns in 2025. These ten funds recorded an average return of 18.1% in 2025*. The one bond fund in the group continues to illustrate that fixed income investments are structurally well suited to pursue sustainable outcomes without sacrificing risk-adjusted returns.

• Across investment categories with assigned quality ratings, four funds have been assigned the highest “A” fund quality ratings. Funds in the leading “A” level rating category are considered leading candidates for positions within diversified portfolios consisting entirely or partially of sustainable funds or on a stand-alone basis.

Observations:

• The ten largest focused sustainable long-term funds, including mutual funds and ETFs, ended 2025 with $127.3 billion in assets under management, accounting for 34% of the segment’s $374.6 billion in assets as of the same date. This was a slight drop from 34.7% at the end of 2024.

• Consisting of nine equity funds, seven US equity funds, two international funds, as well as one fixed income fund, the group comprised of the largest ten funds is equally divided between five actively managed portfolios and the same number of index tracking funds. Included are six Large Blend Funds, one Large Growth Fund, two Foreign Large Blend funds and one Intermediate Core Bond fund. In addition, a range of sustainable investing strategies are covered, but these are dominated by approaches that in varying ways rely on ESG screening and exclusions. That said, sustainable investing strategies also extend to impact or outcomes-based considerations and ESG leadership.

• As a group, these funds posted an average return of 18.1% in 2025* (based on the largest share class for mutual funds), ranging from a low of 7.5% registered by the Nuveen Core Impact Bond Fund R6 to a high of 31.23% achieved by the Vanguard ESG International Stock ETF. This was against a backdrop of strong returns across equity and fixed income markets. The S&P 500 Index produced its third consecutive year of double-digit gains, rising 17.9%, international stocks, based on the MSCI ACWI ex USA index, added 33.1%, while the Bloomberg U.S. Aggregate Bond Index, a benchmark for U.S. government, corporate and mortgage-backed securities, rose 7.30%.

• Expense ratios applicable to the group is an average 0.36% or 36 basis points (bps), falling along a range that extends from a low of 0.1% or 10 bps to a high of 92 bps. At an average of 13 bps, index tracking funds are significantly less expensive than the cohort of actively managed funds with an average expense ratio of 59 bps.

• The line up of the four largest funds remained unchanged at year-end 2025 versus 2024, led by the $25.9 billion Parnassus Core Equity Fund. The fund’s Institutional share class posted a gain of 11.88% and saw its assets decline by $3.3 billion over the course of the year. At the same time, the fund taking up the second spot, the Vanguard FTSE Social Index Fund, registered a gain of 17.3% and closed in on the size gap by adding $2.9 billion during the same time interval.

• The Brown Advisory Sustainable Growth Fund, which was the fifth largest sustainable fund at the end of 2024, fell out of the top ten group. The fund’s Institutional share class, up 3.63% in 2025, lagged its benchmark by a significant margin and experienced a decline in net assets in the amount of $3.5 billion.

• The single bond fund in the group, the actively managed Nuveen Core Impact Bond Fund, moved up a notch to take up the 8th spot. The fund’s largest share class, R6, gained 7.5% and outperformed the Bloomberg US Aggregate Bond Fund. The fund added $518 million in assets. The fund continues to illustrate that fixed investments are structurally well suited to pursue sustainable outcomes without sacrificing risk-adjusted returns.

• For investors, the following four funds are considered leading candidates for core positions within diversified portfolios consisting entirely or partially of sustainable funds or on a stan-alone basis, based on their assigned “A” ratings by Sustainable Research and Analysis. Vanguard FTSE Social Index Fund, Vanguard ESG US Stock ETF, Victory Pioneer Fund (all share classes), and Nuveen Core Impact Bond Fund. Investors should also consider whether these funds align with their sustainable investing preferences as set forth in summary form below.

*Or an average of 19.3% without the inclusion of the single fixed income fund in the group.

Sustainable investing defined

Sustainable investing is an umbrella term that this investing approach through portfolio- and ownership-based methods that encapsulate not only ethical investing, socially responsible investing and responsible investing but also various other strategies or approaches listed below, each with its own set of risks and benefits.

While there is no universally accepted definitions or framework as yet and definitions continue to evolve, today sustainable investing refers to a range of overarching investment approaches or strategies. Most practitioners agree that these encompass the following strategies that may be employed individually or in combination:

Values-based investing. Also referred to as faith-based investing, socially responsible investing, responsible investing, ethical investing or investing based on a set of morals, the guiding principle is that investments are based on a set of beliefs with a view toward achieving a positive societal outcome. Typically, this approach is executed via negative screening, divestiture or divestment.

Negative screening or exclusionary strategies. These involve the exclusions of companies or certain sectors from portfolios based on specific ethical, religious, social or environmental guidelines or preferences. Traditional examples of exclusionary strategies cover the avoidance of any investments in companies that are fully or partially engaged in gambling and sex related activities, the production or manufacturing of alcohol, tobacco or firearms, or even atomic energy. These exclusionary categories have been extended in recent years to incorporate additional considerations, for example, firms that are the subject of serious labor-related actions or penalties by regulatory agencies or demonstrate a pattern of employing forced, compulsory or child labor, or firms that exhibit a pattern and practice of human rights violations or are directly complicit in human rights violations committed by governments or security forces, including those that are under US or international sanctions for grave human rights abuses, such as genocide and forced labor. That said, it should be noted that significant policy shifts and investor sentiment are taking place in North America and Europe regarding the treatment of nuclear energy and the defense sector, driven by recognition of nuclear energy’s role in meeting the dual goals of energy security and net zero emissions while the war in Ukraine has been responsible for shifting the perception and interest among institutional investors in the defense sector.

Closely related is the strategy of divestiture or divestment. Divestiture strategies involve current holdings that are liquidated over time as their eligibility is no longer consistent with the owner’s objectives, such as fossil fuel companies. But divestiture strategies may also involve a much broader universe of securities, such as when for example, divestiture strategies were applied to apartheid practices in South Africa in the 60s and 70s. At that time, any company doing business with South Africa was taken off the list of eligible investments.

Impact investing. Still a relatively small but growing slice of the sustainable investing segment, impact investments are incremental (additional) moneys directed to companies, organizations, and funds with the intention to achieve measurable social and environmental impacts alongside a financial return. Impact investments can be implemented in both emerging and developed markets and made across asset classes, such as equities, fixed income, venture capital, and private equity. In each instance, the objective is to direct capital to address challenges in sectors such as sustainable agriculture, renewable energy, conservation, microfinance, and affordable and accessible basic services, including housing, healthcare, and education.

Historically, impact investments have targeted a range of returns from below market to market rate, depending on the investors’ strategic goals. But increasingly, impact investing strategies are expected to at least achieve risk-adjusted market rates of return.

A less rigorous definition of impact investing, but one that is gaining traction, involves providing direct exposure to issuers, issues, projects or investments that are believed to have potential for achieving social and/or environmental benefits.

Thematic investing. An investment approach with a focus on a particular idea or unifying concept, for example securities or funds that invest in solar energy, wind energy, clean energy, clean tech and even gender diversity, to mention just a few of the leading sustainable investing fund themes. Investing in low carbon emitting stocks and bonds or green bonds or funds also fall into the thematic investing category.

ESG integration. This is a widely practiced investment approach by which environmental, social and governance factors and risks are systematically analyzed and, when these are deemed relevant and material to an entity’s performance, they will influence decisions on whether to buy or hold a security, and to what extent. Such considerations may lead to the liquidation of a security from the portfolio but at the same time, these factors may also identify investment opportunities.

Shareholder advocacy, issuer engagement and proxy voting. These strategies, which leverage the power of stock ownership in publicly listed companies and, regarding engagement, the power of bond investments, are action-oriented approaches that rely on learning about each company’s ESG practices and related risks and opportunities. These strategies also extend to influencing corporate behavior through direct corporate engagement, filing shareholder proposals and proxy voting.

Structural sustainability. The scope for expressing sustainability objectives through security selection or ownership rights in money market funds is inherently limited by regulatory requirements and liquidity mandates. As a result, many sustainable money market fund offerings pursue sustainability objectives through structural mechanisms that operate outside traditional portfolio construction, such as inclusive intermediation practices (e.g., broker-dealer selection and distribution partnerships) and the allocation of adviser revenues to charitable or social purposes. In this analysis, such approaches are characterized as forms of “structural sustainability,” reflecting their focus on market processes and economic flows rather than on portfolio composition or issuer engagement.

Updated 1/17/2026

SRA quality ratings-An Explanation

Fund quality ratings are evaluated and assigned to funds within their designated investment category/segment. Fund quality ratings are expressed along a five-point scale that runs from A (highest quality) to E (lowest quality).

Ratings combine qualitative and quantitative elements and are derived based on an evaluation of the five factors. The first three, which are evaluated qualitatively, are: (a) Management company. The fund should be offered and managed by an established firm with a positive reputation, to ensure effective fund operations and instill trust and confidence in the organization. (b) Years in operation. The fund should be in operation for at least three years and managed pursuant to the same investment strategy—to provide a sufficiently long but not excessively long view against which to evaluate the fund’s operations, strategy, and performance. (c) Fund size. The fund’s total net assets should exceed $30 million—so that it may be managed more efficiently and to provide some protection against the fund’s early liquidation or closure. Some exceptions may apply in the case of funds offered by larger, established firms. The next two factors, which are evaluated quantitatively via a scoring methodology, are: (d) Total returns. The fund’s performance results, achieved by adhering to a relatively consistent investment approach, are evaluated relative to an appropriate securities market index over a one year, three year and five-year intervals, and (e) Expense ratio. The fund’s expense ratio is evaluated relative to other funds in the same investment category/segment.

One evaluated and scored, fund quality ratings are distributed as follows: Top 15%=A, next 20%=B, next 30%=C, next 20%=D and final 15%=E.

NR indicates that a rating has not been assigned to the fund as it employs leverage, it falls outside the designated investment category, or it fails to meet one of the minimum requirements.

Funds with quality ratings in category levels “A” and “B” should be considered leading and secondary candidates for positions within diversified portfolios consisting entirely or partially of sustainable funds or on a stand-alone basis. Leading and secondary candidates should be evaluated relative to an investor’s sustainability preferences. In the case of thematic funds, such as renewable energy funds, investors should keep in mind that some funds are narrowly focused, for example, funds investing in solar or wind energy, while others are broader based, for example, renewable energy or energy transition.

Fund selections should be consistent with an investor’s financial goal and objectives and sustainability preferences.

Updated 1-17-2026